Something interesting has happened to the global property market over the past couple of years. The pandemic disruption, the rate shock, the cost-of-living squeeze — all of it reshuffled where in the world property actually makes sense to own. Some global cities came out of that period quietly stronger. Others are still finding their footing. For Australian investors, the question in 2026 isn’t just “should I invest?” — it’s “where on earth do I invest?” Your dollar goes further in some markets than others.

Your risk sits differently. And your tax position changes completely depending on which passport lane you’re walking through at customs. This is our honest, data-grounded read of the five global cities worth serious attention in 2026. Not hype. Not a brochure copy. Just the real picture.

The five global cities at a glance

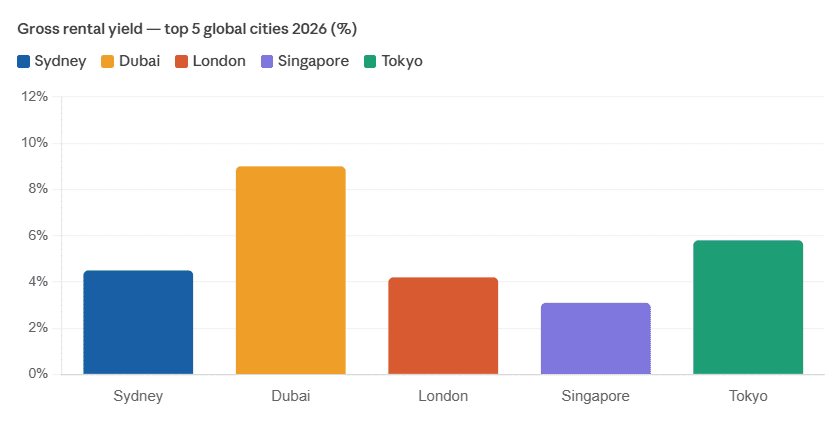

Before we go city by city, here’s what the headline numbers look like side by side.

| City | Gross Yield | Capital Growth (2026) | Min Entry (AUD) |

| Sydney | ~4.5% | ~7.7% | $600K–$1.5M+ |

| Dubai | ~9% | 6–12% | ~$250K+ |

| London | ~4.2% | ~4% | ~$700K+ |

| Singapore | ~3.1% | ~5% | ~$1.1M+ |

| Tokyo | ~5.8% | ~3.5% | ~$280K+ |

The city profiles

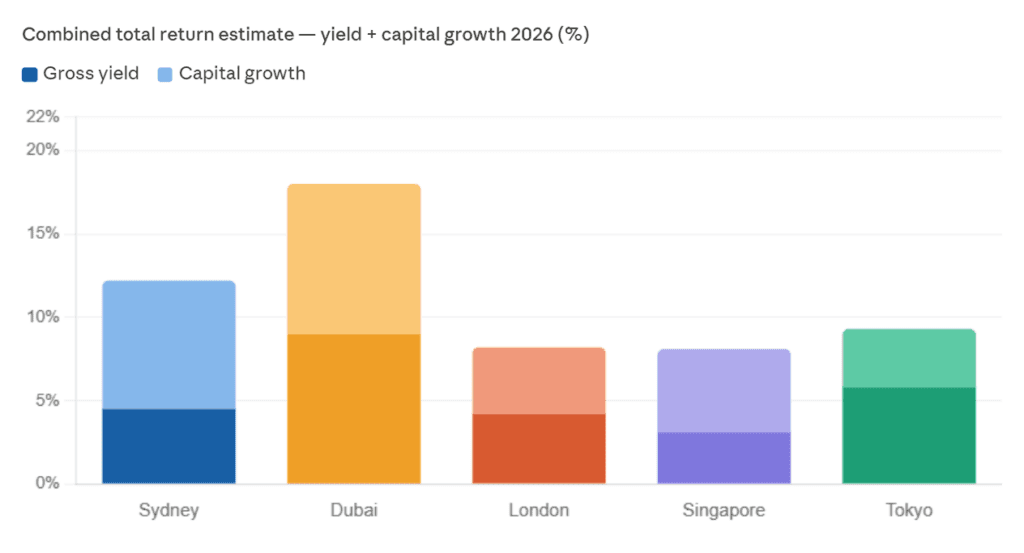

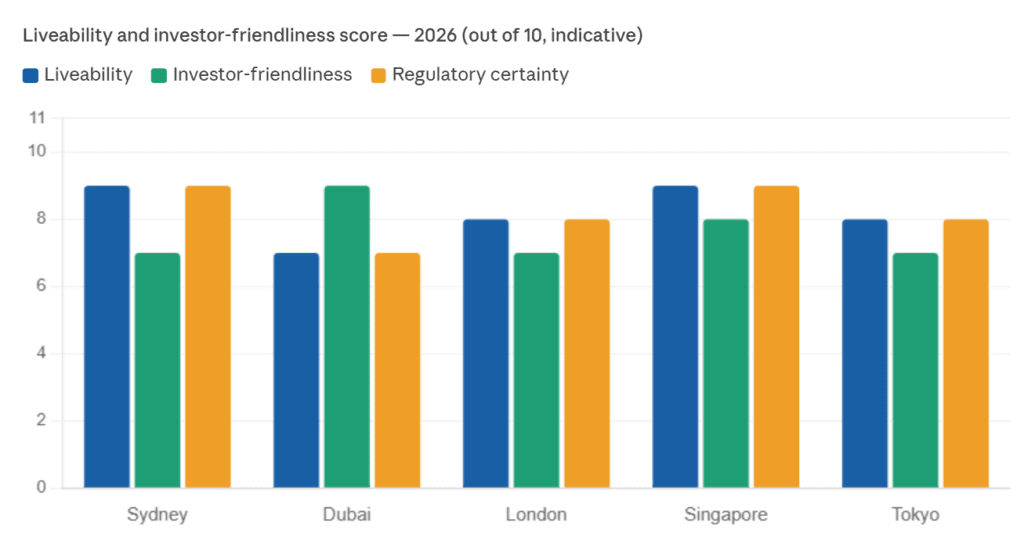

How do they compare across the metrics that matter?

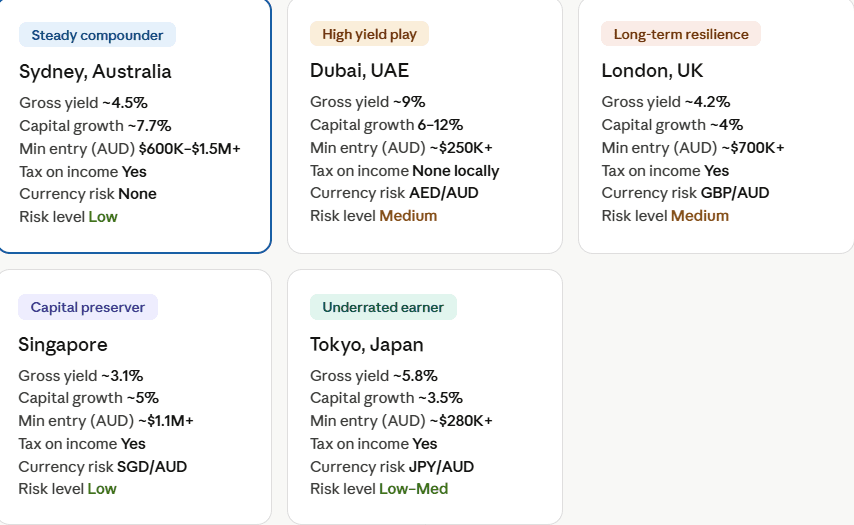

Sydney, Australia — boring in exactly the right way

Sydney doesn’t make headlines for overnight millionaires and it never has. What it does consistently — decade after decade — is compound wealth quietly and reliably. That’s actually the whole point.

In 2026, national house prices are forecast to grow by around 7.7%. Sydney is pulling more than its share of that. The driver isn’t hard to identify: population growth is running ahead of housing supply, and it has been for years. Net overseas migration is still strong. Skilled workers, international students, young families — they all need somewhere to live, and Sydney remains one of Australia’s most preferred destinations.

What makes Sydney uniquely appealing for local investors is everything you can’t put a number on. You know the legal system. You understand the planning rules. You can read a contract without a translator. There’s no currency exposure and no foreign ownership complexity to navigate. For an investor building long-term wealth, that familiarity has genuine value.

The honest downside? Entry prices are high — you’re typically looking at $600,000 at the lower end for an investment-grade property, and well over $1 million in most inner and middle-ring suburbs. Stamp duty hurts. And gross yields of 4–5% look modest compared to what’s available offshore.

Sydney is built for the patient investor. It’s not where you go to chase a headline yield. It’s where you go to build something that holds.

Dubai, UAE — the yield story that keeps getting harder to ignore

The residency visa pathways have expanded. And the city has attracted a genuinely international tenant base — professionals, entrepreneurs, digital nomads — who rent year-round and pay reliably.

The yield numbers are the headline: 8–10% gross rental returns. More than double what Sydney’s inner suburbs are generating. And that’s before you account for Dubai’s tax position. There’s no local rental income tax and no capital gains tax on property. For an Australian investor used to handing a significant portion of rental income straight to the ATO, the difference in what actually lands in your account is substantial.

Off-plan payment structures add another layer of appeal. Many Dubai developers allow staged payments during construction, which means you can control a meaningful asset with a smaller upfront commitment. And if you buy above certain thresholds, you may qualify for the UAE Golden Visa — long-term residency as a byproduct of your investment.

The counterpoint is real though. Dubai’s market is more volatile than Sydney’s or Singapore’s. Price movements can be sharper and faster. You’re managing an asset remotely, in a legal and cultural framework that differs meaningfully from Australia’s. And while Australian residents still need to declare Dubai rental income to the ATO, foreign tax credits help navigate the double-taxation exposure.

Dubai is the right city for investors who’ve done the homework, built the local team, and can absorb some volatility in exchange for materially better income.

London, UK — quiet confidence after a rough few years

London had a difficult stretch. Price corrections, regulatory changes, post-Brexit uncertainty, and the added burden of new landlord obligations made it a less comfortable market than it used to be. But in 2026, the London property market is finding solid footing again — and that’s creating some of the best relative value the city has offered in years.

The fundamentals haven’t changed. London is still one of the world’s leading financial centres, an internationally ranked education hub, and a cultural destination that draws migrants and students in enormous numbers. Prime and near-prime areas that saw price adjustments over the past few years are now looking genuinely interesting compared to their historical highs.

Rental demand is consistent and year-round, driven by young professionals, international students, and long-term renters in well-connected zones. Gross yields in the 4–4.5% range aren’t going to excite anyone chasing Dubai numbers — but the stability and depth of the London rental market is hard to replicate.

For Australian investors, the complexity sits in the GBP/AUD exchange rate exposure and UK tax obligations. Non-resident landlord rules apply, stamp duty for foreign buyers is higher, and the regulatory environment for landlords has been tightening. This is a market that rewards investors who invest time in understanding it before putting capital in.

Singapore — capital preservation, not income generation

Singapore is unique on this list. It’s not where you go for yield. It’s not where you go for entry-level affordability. It’s where capital goes when it needs to be preserved with high confidence in a politically stable, rigorously governed environment.

The fundamentals are strong: limited land supply, strict planning controls, a world-class financial hub, excellent governance, and growing relevance as Asia’s primary business and wealth centre. These are conditions that support steady, long-term price appreciation.

But Australian investors need to understand the stamp duty reality upfront. As of 2025, foreign buyers face an Additional Buyer’s Stamp Duty (ABSD) of 60% on top of the purchase price. That number is not a typo. It makes the yield and growth story almost impossible to justify on traditional investment metrics for most Australians. At a gross yield of around 3.1% and price growth of roughly 5%, the return doesn’t absorb a 60% entry cost in any timeframe that makes practical sense.

Singapore belongs on this list because it matters globally and because institutional and ultra-high-net-worth investors still find value in it — particularly those seeking residency, wealth preservation, or strategic Asia-Pacific positioning rather than return maximisation.

Tokyo, Japan — the most underrated market on this list

Tokyo rarely comes up in conversations about global property investing. That’s precisely why it’s interesting.

Compared to every other city on this list, Tokyo’s entry costs are remarkably low — investment-grade properties accessible from approximately AUD $280,000 in central locations. Gross rental yields sit around 5.8%, which is better than Sydney and London and competitive with the broader U.S. market. Vacancy rates in central wards are low, tenant culture is reliable, and the purchase process for foreign investors is genuinely straightforward.

The weak yen has amplified Tokyo’s appeal for international buyers over the past couple of years. When your dollar buys more yen, you’re acquiring quality assets at a discount to their real-world value — and that enhanced entry point improves your effective yield without changing anything about the asset itself.

What Tokyo doesn’t offer is explosive capital growth. Japan’s broader demographic trends — an ageing population, declining birth rates — keep a lid on national price pressure. You’re investing for steady income and modest appreciation, not a rapid doubling of asset value. For investors who want reliable, consistent returns from a well-governed market with low management friction, that’s not a bad deal at all.

How to choose the right city for you?

- Yield chasers who want maximum income and can manage offshore complexity — Dubai, followed by Tokyo.

- Long-term compounders who want capital certainty and a familiar system — Sydney, without question.

- Patient contrarian investors who believe in structural resilience — London, particularly in the current window.

- Capital preservers with significant net worth and an Asia-Pacific strategy — Singapore, with full awareness of the stamp duty reality.

Quiet, consistent earners who want offshore diversification without drama — Tokyo, particularly while the yen remains weak.

Full comparison table

FAQs

- Can Australians buy property in all five of these global cities?

Yes, but with different rules in exach market. Sydney has no restrictions for locals. Dubai is fully open to foreign buyers in designated freehold zones. London allows foreign purchases freely. Singapore has the most restrictive rules — foreigners pay an ABSD of 60%, which dramatically changes the investment case. Tokyo is genuinely open and foreigner-friendly with no special restrictions. - Which city is best for rental income right now?

Dubai, by a clear margin — 8–10% gross yields and no local rental income tax make it the strongest pure income play. Tokyo comes second at around 5.8% gross with stable vacancy rates. Sydney and London are more capital-growth stories at current price levels. - Do I pay Australian tax on income from overseas property?

Yes. The ATO taxes Australian residents on worldwide income, including rental income from Dubai, London, Singapore, or Tokyo. Foreign tax credits may offset taxes paid overseas, but you are still required to declare it all. The interaction between foreign and Australian tax obligations is complex — get specialist advice before assuming the maths work in your favour. - Is Singapore worth it given the 60% stamp duty for foreign buyers?

For most Australian investors, the numbers don’t work. That ABSD makes direct ownership very difficult to justify on yield or growth grounds. Singapore’s appeal sits with ultra-high-net-worth investors focused on capital preservation and residency strategy rather than return maximisation. - Why is Tokyo so affordable compared to other global capitals?

Japan’s population dynamics, a weak yen, and the absence of speculative investor pressure that drives prices in Sydney or London all contribute. That combination keeps prices relatively modest — which is exactly what makes it interesting for value-oriented investors. - Which city is best for a first-time overseas investor?

Tokyo or Dubai, depending on your priorities. Tokyo offers lower entry costs, stable tenancy, and a straightforward purchase process. Dubai offers higher yields and a growing community of Australian investors who’ve already navigated it. Both are more accessible than London or Singapore for first-timers building an offshore portfolio. - What about currency risk when investing offshore?

It’s real and it matters. A 10–15% shift in AUD against GBP, JPY, or SGD can meaningfully change your effective return — in either direction. The AED is pegged to the USD, so AUD/AED risk mirrors AUD/USD risk. Investors committing significant capital to any offshore market should factor exchange rate scenarios into their return projections and consider whether to hedge.

The NextHouse View

Every city on this list has something genuine to offer — but they don’t all offer the same thing, and that distinction matters enormously. Sydney remains the benchmark for risk-adjusted property returns for Australian investors who want capital certainty and a system they understand inside out. Dubai is a genuinely compelling income play for investors who’ve done their homework and can manage the volatility. London is for patient, long-term thinkers who understand that resilience and global status don’t fade quickly.

Singapore rewards capital preservation over yield chasing — it’s a wealth-protection play, not an income play. And Tokyo is quietly one of the more interesting underappreciated markets in the world right now, particularly while the yen remains weak. The smartest investors in 2026 aren’t picking the city with the biggest number. They’re picking the city that fits their timeline, their tax position, their risk tolerance, and their ability to manage an asset from where they’re sitting. That fit matters more than any yield figure on a chart.

Disclaimer

Before you close this tab and start running numbers, there’s something worth saying clearly. Everything in this article is here to inform — not to advise. NextHouse.com.au puts this content together because Australian investors deserve access to clear, honest, data-driven information. But information is not the same as advice, and this article is not a substitute for professional guidance tailored to your personal circumstances. Property investment carries real risk, including the possibility of losing capital.

All yield figures, growth estimates, and market comparisons are based on publicly available data as of early 2026 — they are our best reading of the numbers right now, but markets move and things change. Past performance does not guarantee future results. Before making any investment decision — particularly one involving overseas markets, foreign currencies, or unfamiliar legal structures — please speak to a qualified financial adviser, a tax accountant with cross-border expertise, and a legal professional familiar with the jurisdiction you’re entering. That advice costs a fraction of what getting it wrong can.

And for the record: NextHouse.com.au is fully independent. We do not receive commissions from property developers, real estate agents, or any third party involved in selling property. Our only interest is giving you a clearer, more honest picture of how these markets actually work.