Ask ten property investors in Australia whether you should buy new vs established homes, and you’ll get ten different answers — most of them shaped by whatever the person in front of you happens to own.

The new build enthusiast will lead with depreciation and low maintenance. The established home devotee will come back with land value and proven suburbs. Both will sound completely convincing. And both will quietly skip the parts that don’t support their case.

So here’s a version that doesn’t do that. One that looks at both sides honestly — because the right answer genuinely depends on what you’re trying to do with your money, and there’s no point pretending otherwise.

New vs Established Homes: What We’re Comparing?

A new home is a freshly built property — either purchased off the plan while it’s still under construction, or as a completed house-and-land package in a newer development. Everything in it is brand new, built to current standards, and covered by a builder’s warranty.

An established home is one that’s already had a life before you came along. It might be ten years old or it might be sixty. It sits in a suburb with its own identity — schools, shops, transport, the lot. You can walk through it, assess its bones, check what similar properties have rented for, and have a tenant in it within weeks of settlement.

That’s the comparison. And both are legitimate investment choices depending on what you’re after.

What New Homes Do Better?

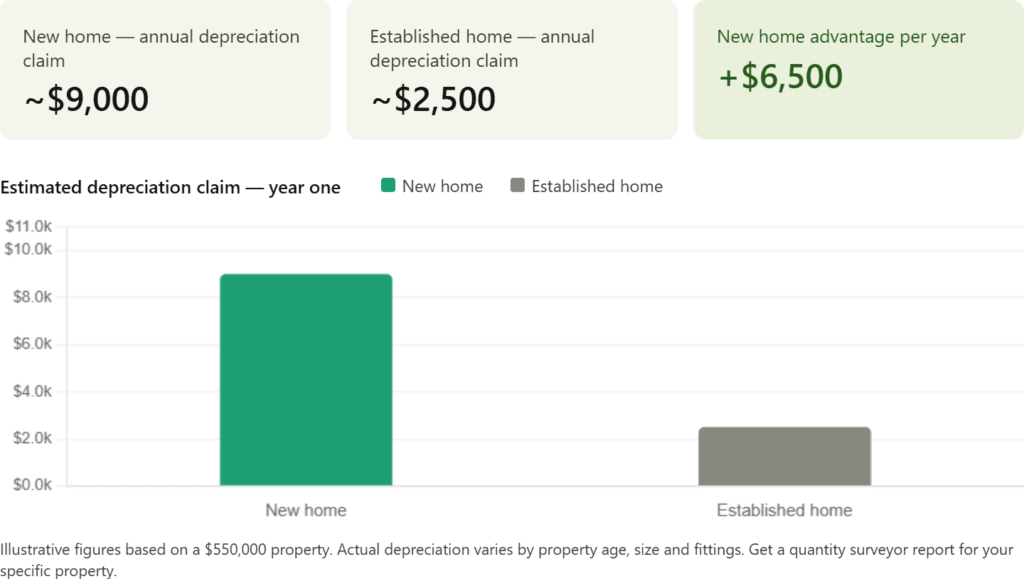

The depreciation advantage is genuinely significant

Of everything in the new home column, this is the one that deserves the most attention — and it’s also the one that gets explained most poorly. When you own an investment property in Australia, the tax system lets you claim depreciation as a deduction each year. Think of it as the government acknowledging that buildings and their contents wear out over time, and giving you a tax break to reflect that. The fresher the property, the more there is to claim. It’s not a gimmick. It’s a legitimate, widely used part of the Australian tax system, and it’s one of the clearest financial advantages new properties hold over older ones.

Maintenance is predictable — at least for a while

Buying new means buying certainty, at least in the short term. Everything is fresh, covered by a warranty, and unlikely to cause you grief for the first several years. No ageing hot water systems. No roof repairs. No plumbing surprises at the worst possible moment.

For investors who are already managing a mortgage and don’t want unpredictable costs eating into their cash flow, this kind of stability is worth more than it might sound. It lets you plan properly instead of holding your breath every time a tenant calls.

Modern properties attract tenants more easily

This one is fairly simple. A lot of tenants — particularly younger renters and professionals — gravitate toward properties with open plan living, decent storage, energy-efficient appliances, and finishes that don’t feel dated. New homes tick those boxes immediately.

Rents in those areas also tend to move upward gradually as demand keeps building and supply stays tight. Nothing about property is ever guaranteed, of course. But this particular pattern has repeated itself across enough suburbs and enough market cycles that it’s hard to dismiss.

What Established Homes Do Better?

The land is what actually grows in value

Buildings get older. They depreciate. The land they sit on does the opposite — particularly in suburbs where there’s no room left to build and demand keeps growing regardless. Established homes in well-located, tightly held suburbs tend to sit on more valuable land in areas where new supply simply can’t materialise. When a suburb has been fully developed for thirty years, no developer can flood it with new stock. Every person who wants to live there has to compete for what already exists.

That’s what drives long-term capital growth, and it’s why established homes in desirable areas have historically outperformed newer developments on the city fringe over any meaningful time horizon. The building matters less than people think. The land it sits on matters enormously.

Income starts immediately after settlement

Off-the-plan purchases in particular carry a timing problem that doesn’t get flagged loudly enough: there’s often a significant gap between when you signed the contract and when you can actually put a tenant in. Construction runs late. Handover gets pushed back. During all of that, loan repayments are ticking along without any rent coming in to offset them.

With an established home, you settle and you’re done. Your property manager can have it listed and tenanted within weeks. For investors who need that rental income to service the loan from the start — which is most people — this is a practical advantage with real financial consequences.

You can add value and manufacture equity

This is one of the most compelling things established homes offer that new builds simply can’t match. A dated kitchen, a tired bathroom, original flooring — these are liabilities for a vendor and leverage for a smart investor.

Targeted renovations can lift rental returns, attract better long-term tenants, and build equity at a pace that outstrips waiting for the market to do it for you. It’s not effortless — it takes planning, a realistic budget, and decent decision-making on what to spend and what to leave alone. But when it’s done well, the returns can be meaningful.

You’re buying based on real history, not someone’s forecast

Developer projections are optimistic by design. That’s not a criticism — it’s just the reality of how they’re produced.

With an established property, none of that uncertainty exists. You can see what it rented for, how long it sat vacant between tenants, what the street has done over the last decade. That’s actual evidence, and it gives you a much more honest foundation for making a financial decision than a glossy brochure with growth projections for a suburb that’s still being built.

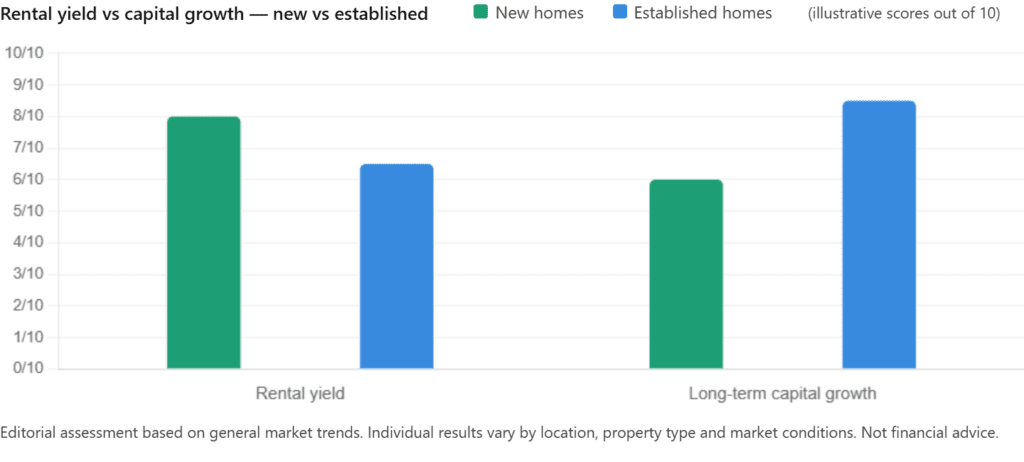

Rental Yield vs Capital Growth — Understanding the Real Trade-off

These two things don’t usually move in the same direction, and getting clear on which one matters more to you is the most important decision in this whole conversation.

Rental yield is income — what the property earns as a percentage of what it costs. New homes in growth corridors tend to do better here, at least in the early years, because their modern appeal keeps vacancy low and rents competitive.

Long-term capital growth in Australian property comes down to one thing more than anything else: land. These areas are already built out. Infrastructure is in place. The people who want to live there keep wanting to live there, and there’s no new supply arriving to take the pressure off prices. That combination is what pushes values up steadily over time, and it’s why location matters so much more than the age of the building.

The honest summary: if you need income now, new homes are generally stronger. If you’re building wealth over a decade or more, established homes in the right locations tend to win on the numbers that matter most.

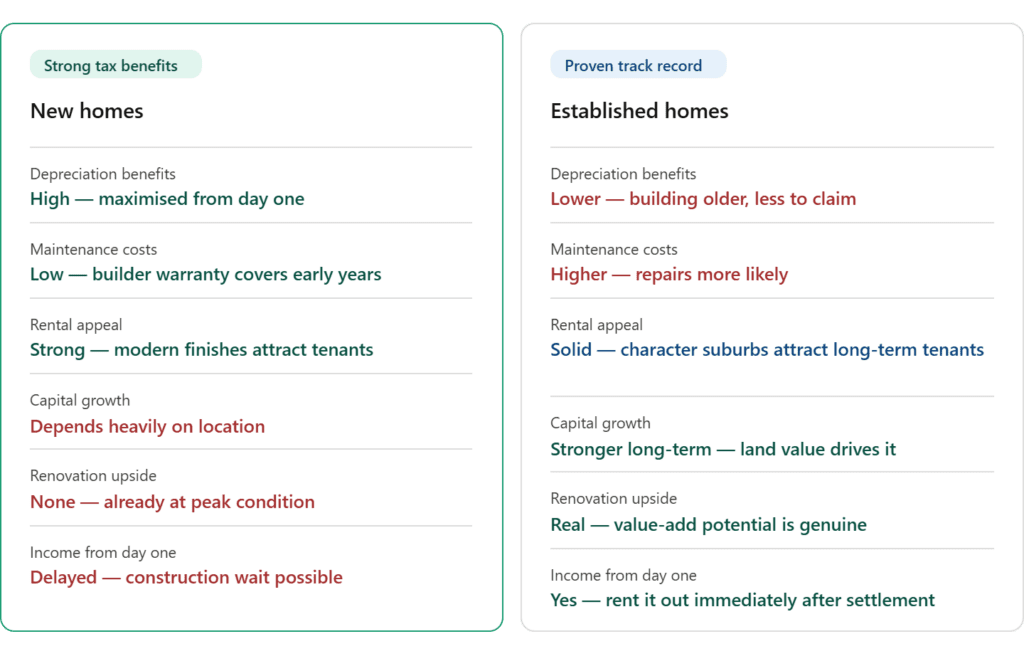

Full Comparison at a Glance: New vs Established Homes

So Which One Is Actually Right for You?

New homes make more sense when you want strong cash flow and tax benefits working in your favour from the start, you’re comfortable buying in a newer growth area without a long established track record, low maintenance and warranty protection matter to you, and the depreciation benefit is a meaningful part of your financial strategy.

Established homes make more sense when you’re investing for the long haul and land value appreciation is your primary goal, you want to generate rental income from the moment you settle, you see renovation potential as an opportunity rather than a hassle, and you want to make your decision based on real data rather than developer projections.

New vs Established Homes— the investors who tend to build the most resilient portfolios over time don’t pick a side and stay there. They hold both. A newer property generating strong cash flow and depreciation benefits alongside an established property in a well-located suburb quietly compounding in value over a decade. That combination manages risk and captures returns from both ends of the spectrum at the same time.

Ready to work out which type of property suits your goals in 2026? Get in touch with NextHouse — we’ll help you cut through the noise and find what actually makes sense for you.

Disclaimer: This report is for educational and informational purposes only. It does not constitute financial, investment, or legal advice. Always seek professional advice before making property decisions.