If you’ve spent any time in a first home buyer Facebook group or read a finance newsletter recently, you’ve seen the word rentvesting. It sounds like a buzzword. And to be fair — it kind of is. But underneath the marketing, it describes a real strategy that a growing number of Australians are using to get into the property market without giving up the suburb they actually want to live in.

This guide explains what rentvesting actually is, walks through the full financial picture — including the parts most blogs quietly skip — and helps you work out whether it makes sense for your situation.

No cheerleading. No scare tactics. Just the data, clearly explained.

1. What is Rentvesting?

Rentvesting is when you rent the home you live in — in a suburb you love — while simultaneously owning an investment property somewhere else that makes better financial sense. That’s it. There’s no special loan product, no government scheme called “rentvesting,” and no magic trick involved. It’s standard investment property ownership — the framing is just different. Instead of saving for a decade to buy in your dream suburb, you buy where the numbers work and keep renting where life works.

The key insight: If buying where you want to live requires 14 years of saving — like it does in Sydney — rentvesting lets you get into the market now, build equity somewhere more affordable, and stay in the suburb that suits your life.

Rentvestor profiles. Not all of these suit every situation — see Section 10 for the suitability framework.

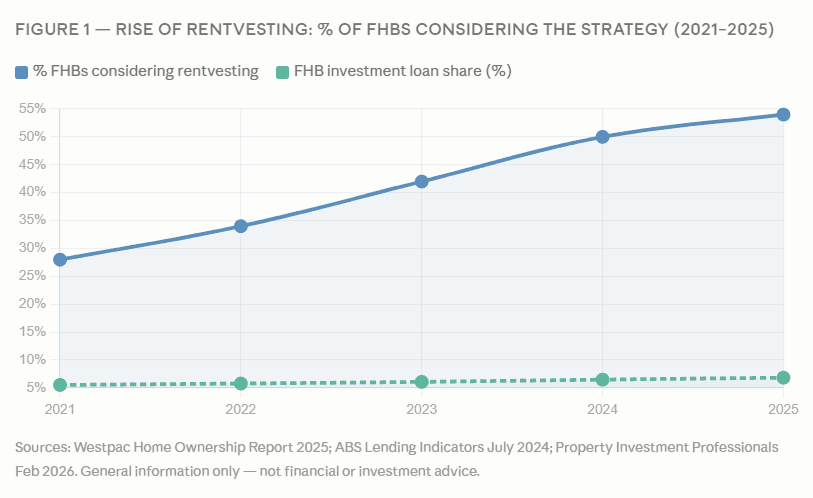

2. The data: why rentvesting is everywhere in 2026

This isn’t just anecdote. The data shows rentvesting has moved from a niche workaround to a genuine mainstream option for first home buyers.

- 54% of first home buyers are now considering rentvesting (2025) — up from 50% in 2024

- 61% of FHBs in NSW considering rentvesting — the highest of any state

- +25% increase in FHBs choosing investment loans since July 2019 (ABS)

- 21.4% rentvesting loan growth vs 9.1% for standard owner-occ FHB loans (Feb 2026)

They’re not manufactured. The structural logic — rent where I want to live, invest where the numbers work — is a rational response to a market where affordability and lifestyle have pulled sharply apart.

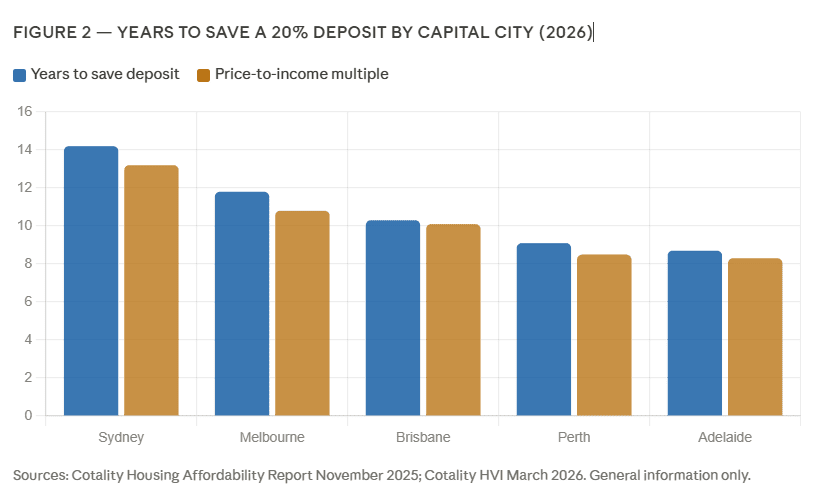

3. The affordability problem that’s driving it

Rentvesting doesn’t exist in a vacuum. It has grown in direct proportion to how unaffordable Australian cities have become. You can’t understand the strategy without understanding the context.

Australian home values have risen 47.3% since the COVID lockdowns of 2020 (Cotality, November 2025). On a median household income, saving a 20% deposit now takes more than a decade in most capital cities. In Sydney, it takes over 14 years.

Affordability data by capital city. Sources: Cotality Housing Affordability Report November 2025; Cotality HVI March 2026.

When buying where you want to live requires sacrificing an entire decade of savings, the question “what are the alternatives?” stops being theoretical.

| City | Approx. median house price | Years to save 20% deposit | Price-to-income multiple |

| Sydney | AUD 1,400,000+ | 14.2 years | 13.2x household income |

| Melbourne | AUD 960,000 | 11.8 years | 10.8x household income |

| Brisbane | AUD 1,000,000+ | 10.3 years | 10.1x household income |

| Perth | AUD 780,000 | 9.1 years | ~8.5x household income |

| Adelaide | AUD 770,000 | 8.7 years | ~8.3x household income |

| National average | Various | More than a decade | 8.4x household income |

4. How rentvesting actually works, step by step

The process takes proper planning, but it’s not complicated when you understand the moving parts. Here what you all need to know—

- Step 1: Decide your lifestyle location — close to work, friends, amenities. You’ll be a tenant here.

- Step 2: Find an investment location — a different suburb, city, or region where property fundamentals (yield, growth, entry price) are stronger than where you want to live.

- Step 3: Buy the investment property on a standard investment home loan. You’re the landlord. A tenant lives there and pays you rent.

- Step 4: Rent the home you live in from another landlord. You’re the tenant.

- Step 5: Manage the ongoing cash flows — rental income coming in, loan repayments going out, your own rent going out, and any negative gearing tax offset coming back at tax time.

- Step 6: Build equity over time. Eventually use it to buy your own home, add another investment, or move into the investment property itself.

Table 3: What to look for in a rentvestor’s investment property. General guidance only — not personalised financial advice.

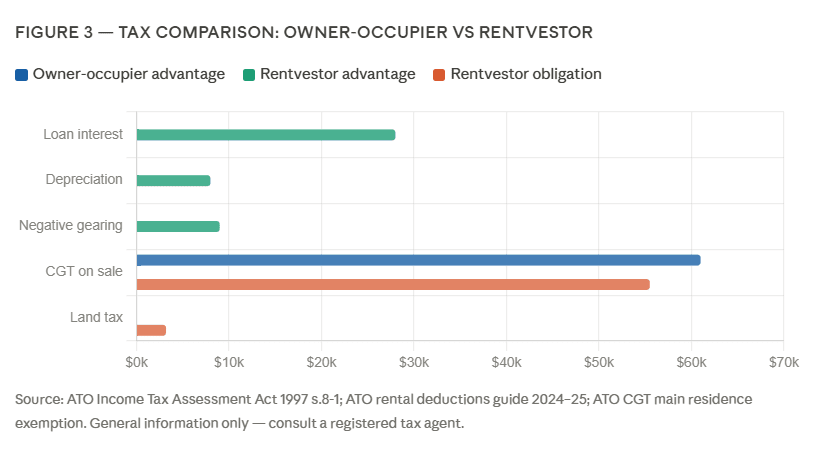

5. The tax side — what you gain and what you owe

Tax is one of the most talked-about parts of rentvesting — and one of the most misunderstood. There are real advantages. There are also real obligations. You need both sides of the picture.

What can you claim?

If your total deductible expenses exceed your rental income, the property is negatively geared. That net loss can be offset against your salary — reducing your taxable income and potentially returning part of the loss at your marginal tax rate.

What you owe — the CGT obligation

When you sell your investment property, Capital Gains Tax applies. There’s no main residence exemption. You do get the 50% CGT discount if you hold for more than 12 months. But on a significant gain, it’s still a real tax bill.

Illustrative example (not advice): At 37% marginal rate: approximately $55,500 in CGT. If that had been your own home, the $300,000 gain would’ve been completely tax-free. Always consult a registered tax agent.

The 6-year rule

If you live in the investment property for at least 12 months before renting it out, you can elect to treat it as your main residence for CGT purposes for up to six years while renting elsewhere. This can eliminate or significantly reduce your CGT bill if you eventually move in.

Tax treatment comparison. Source: ATO. General information only — consult a registered tax agent.

| Tax item | Owner-occupier | Rentvestor |

| Loan interest deductibility | Not deductible | Fully deductible against rental income + other income |

| Depreciation deductions | Not available | Available (new builds or QS report) |

| Negative gearing offset | Not applicable | Net rental losses offset against salary/wages |

| Capital gains tax on sale | Nil — main residence exemption | CGT applies — 50% discount if held 12+ months |

| Land tax | Exempt (primary residence) | Applies above thresholds (varies by state) |

| Stamp duty | FHB concessions if eligible | Full standard rate — no FHB concessions |

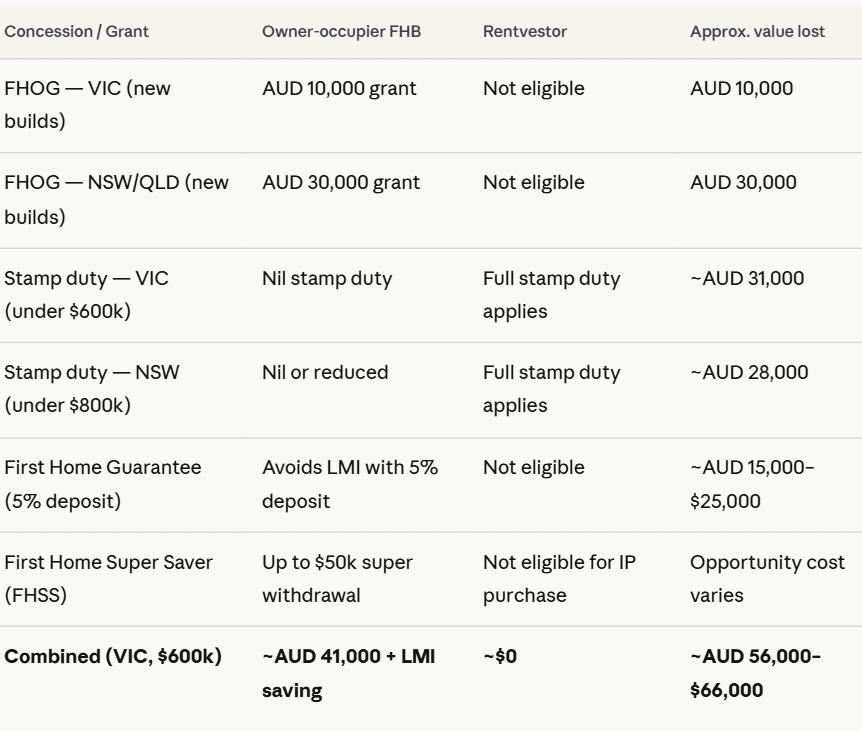

6. What you give up — government grants and concessions

This is the section most rentvesting content glosses over. When you buy a property as an investor — even if it’s your first property ever — you’re not a “first home buyer” for the purposes of most government concession programs. The financial gap is significant.

The grants gap — Victoria example: In Victoria, the combined value of the First Home Owner Grant ($10k), stamp duty exemption (~$31k on a $600k property), and LMI saving via the First Home Guarantee (~$20k) totals approximately $61,000 for an eligible owner-occupier FHB. A rentvestor buying the same property forfeits all of it. That $56,000–$66,000 gap is the single most important number any Victorian rentvestor needs to factor into their calculations.

Government concessions summary. Sources: SRO Victoria; Revenue NSW; NHFIC. Figures approximate — verify with state revenue offices.

Important exception: In Victoria, if you’ve never lived in a property you owned for 6+ months, you may still be eligible for the FHOG on a future owner-occupied purchase — even after previously rentvesting. Always verify with the State Revenue Office Victoria.

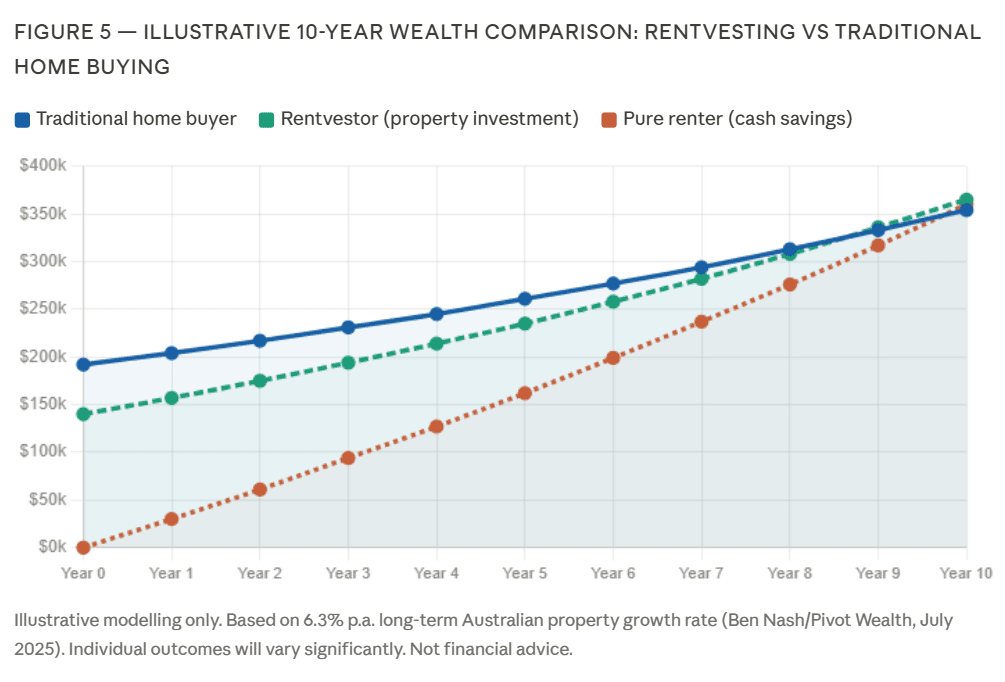

7. Rentvesting vs buying your own home — the numbers

The financial comparison is genuinely complex. The outcome depends on the relative growth rates of the suburb you rent in versus the suburb you invest in, the rent-to-mortgage gap, your tax offset, and the CGT bill on exit.

Financial adviser Ben Nash ran a 10-year comparison using Australia’s long-term property growth rate of 6.3% per annum. He found that buyers who purchase their own home come out approximately $116,120 ahead over 10 years compared to a pure rent-and-save strategy — but the gap narrows significantly when the renter is also investing in property.

The key variable: The critical factor is the relative capital growth between the suburb you rent in and the suburb you invest in. If your target lifestyle suburb grows faster than your investment suburb, rentvesting will likely underperform traditional home buying. If your investment suburb grows at a similar or higher rate while offering a lower entry price and better yield, rentvesting can build more total wealth.

Financial comparison inputs (2026). Illustrative figures only — not financial advice.

8. Where are Australians investing as rentvestors in 2026?

| Live in (rent) | Invest in | The logic |

| Inner Sydney | Brisbane, Adelaide, outer Perth | Sydney entry $1.4M+. Brisbane/Adelaide under $700k with 4%+ yield and strong growth. |

| Inner Melbourne | Brisbane, Adelaide, Melbourne outer-ring | Melbourne core is expensive. Sunshine, Reservoir, outer-west offer $600–800k entry with better yield. |

| Any capital city | Sunshine Coast, Geelong, regional VIC | Lifestyle markets with strong population inflow. Lower entry than capitals. |

Common rentvestor live-and-invest combinations (2026). General guidance only.

- Brisbane (QLD): API Magazine named Brisbane a top pick for rentvestors in 2026 — yields of 3.8–4.5% combined with ongoing price growth underpinned by population inflow and infrastructure spending.

- Adelaide (SA): Highest FHB investment loan share after NSW. Strong yield-growth combination. Entry under $700k in many growth precincts..

- Geelong (VIC): Regional market with Melbourne connectivity, family demand, and $600–750k entry prices.

- Perth (WA): Strong recent growth. Entry below $800k in many suburbs. Caveat: Perth is the most cyclical Australian market — timing matters more here than in other capitals.

9. The honest risks — what can go wrong?

- Vacancy risk: When your investment property sits empty, you still pay the mortgage, rates, insurance, and body corporate. On a $600,000 loan at 6.75%, that’s approximately $780/week in interest alone. A six-week vacancy can cost $4,700+ with no offsetting rental income.

- Rent increase risk: You’re a tenant. Your landlord can increase your rent. Your lease can end. You can be asked to vacate with 90 days’ notice. The stability of owning your own home is real and significant — and rentvesting doesn’t give you that.

- The psychology problem: Some rentvestors in 2026 find the strategy works financially but creates ongoing anxiety about not owning the home they live in. The Australian cultural association between homeownership and security is deeply embedded. Financial models don’t capture that.

- The dual cost burden: You’re paying rent to live somewhere and servicing a mortgage somewhere else. If the investment is negatively geared, the shortfall comes out of your income — on top of your own rent.

- Interest rate risk: The RBA raised the cash rate to 3.85% in February 2026. Investment property loan rates typically run 0.5–0.7 percentage points above owner-occupier rates.

- APRA lending restrictions (2026): Investment loans require larger deposits, higher serviceability buffers, and are assessed at investment rates — meaning borrowing capacity for rentvesting is typically lower than for an equivalent owner-occupier purchase.

10. Is rentvesting right for you?

Rentvesting tends to make sense when:

- The deposit required to buy in your lifestyle suburb requires 10+ years of saving on your income.

- Your investment suburb offers at least 4% gross yield and real growth potential.

- The rent you pay to live is significantly cheaper than the mortgage you’d pay to own in the same area.

- Your income is stable enough to manage both rent and investment loan shortfalls.

- Your investment horizon is 7+ years — long enough for growth to compound and CGT to become proportionally smaller.

- You’re comfortable being both a tenant and a landlord at the same time.

- In NSW: your target lifestyle suburb is above $800,000 (where stamp duty concessions are minimal anyway).

Rentvesting tends not to make sense when:

- The gap between your rent and the equivalent mortgage is small (under $100/week) — the complexity isn’t worth it.

- You’re eligible for substantial FHB concessions — especially in VIC under $600k. That $61k gap is too large to ignore.

- You need lifestyle stability — children in school, care responsibilities, settled community.

- Your target lifestyle suburb has stronger growth prospects than any affordable investment alternative.

- Your income can’t comfortably absorb a 4–6 week vacancy in the investment property.

- You have a short time horizon (under 5 years) — CGT on exit plus stamp duty on entry may eat the gain.

Conclusion

Rentvesting is a legitimate, data-supported strategy for a specific profile — high income, mobile, long time horizon, stable cash flow, willing to be a landlord, priced out of their aspirational suburb by a wide margin, and investing somewhere with credible fundamentals. That is not everyone. It’s a strategy, not a shortcut. When the costs are modelled honestly and the risk profile matches — it can work very well. When they’re not, it’s just paying for lifestyle at the cost of financial security.

Thinking about rentvesting? Get the full picture first.

NextHouse guides independent, data-backed analysis on Australian property — no agent fees, no commissions, no affiliate links. Just the research, clearly explained for investors who want to make informed decisions.

FAQs

- Is rentvesting harder to get approved for than a standard first home buyer loan?

Generally, yes — for a few reasons. As an investor, you need a minimum 10–20% deposit (the First Home Guarantee’s 5% deposit scheme only applies to owner-occupiers). Investment loan rates are typically 0.5–0.7 percentage points higher than owner-occupier rates, which affects serviceability. - Can I still get the First Home Owner Grant if I rentvest first?

Purchasing as an investor generally means you’re not eligible for the FHOG at the time of purchase. However, in Victoria, if you’ve never lived in a property you owned for six months or more, you may still be eligible for the FHOG on a future owner-occupied purchase — even after previously rentvesting. Always verify with the relevant State Revenue Office. - Is rentvesting actually tax-effective?

Rentvesting has genuine tax advantages — interest deductions, depreciation, and the ability to offset rental losses against salary. But it also carries a significant tax obligation on exit: CGT applies when you sell. At lower income levels, the negative gearing offset is smaller because your marginal rate is lower. Always consult a registered tax agent. - Do I need a property manager, or can I manage the investment myself?

Legally, you can self-manage. In practice, most rentvestors in 2026 use one. A property manager handles tenant screening, lease agreements, rent collection, maintenance coordination, routine inspections, and compliance with state tenancy law — which changes regularly. Their fee (typically 7–10% of gross rent) is fully tax-deductible.

Disclaimer: This article is published by NextHouse.com.au for general information and educational purposes only. It does not constitute financial advice, investment advice, property advice, legal advice, or taxation advice.

The author, Ankur, is an independent property analyst and founder of NextHouse.com.au. He is not a licensed financial adviser, registered tax agent, licensed real estate agent, or buyer’s advocate. NextHouse.com.au holds no AFSL, ACL, or real estate licence in any Australian state or territory. Tax laws are complex and change frequently. The tax information in this article is general information only. Individual tax outcomes will vary significantly based on income, property, loan structure, and personal circumstances. Always consult a registered tax agent and licensed financial adviser before implementing any property strategy.

All property investment involves risk, including loss of capital. Past performance is not a reliable indicator of future results.