There’s a question most property investors in Australia never ask before they buy. Not which suburb. Not which lender. Not even which property manager. Something far more fundamental — Company vs Personal Name.

And it gets skipped almost every single time. Whose name goes on the contract? People will spend months researching the right area, drive past a street six times before making an offer, lose sleep over whether to fix the rate or go variable. All of that energy, all of that careful thinking — and then the contract lands, and they sign it in their own name because that’s what everyone does and nobody told them there was another option worth considering.

Here’s the thing though. That one line on a legal document shapes your tax situation, your asset protection, and your long-term financial position for as long as you hold that property. It’s worth five minutes of proper thought before the pen goes down.

What Are the Two Options: Company vs Personal Name?

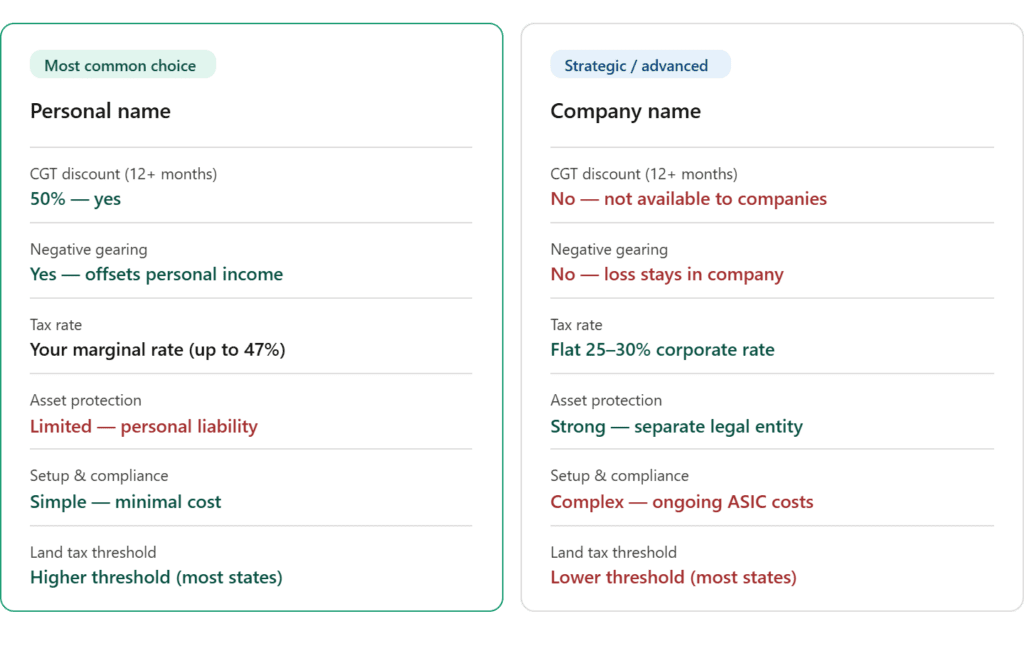

When you buy property in Australia, you can hold it in one of two main ways. The first is your personal name — the way most investors do it, and for good reason. Simple, straightforward, and comes with some genuinely valuable tax benefits built into the Australian system.

The second is under a company structure — a separate legal entity that owns the property independently of you as an individual. More complex, more costly to set up and maintain, but with its own set of advantages depending on what you’re trying to do.

Buying in Your Personal Name — The Case For It

For most Australian investors — particularly those buying their first or second investment property — personal ownership is the stronger starting point. Here’s why.

The 50% CGT discount is a genuinely big deal

This one alone tips the scales for a lot of investors. If you hold a property in your own name for more than 12 months and then sell it at a profit, the Australian tax system only counts half of that gain as taxable income. The other half disappears entirely.

A company gets no such discount. It pays tax on the full $200,000 gain at the corporate rate — around $60,000 at 30%. On a single sale, that’s a $13,000 difference. Over a portfolio and a lifetime of investing, those differences compound into something significant.

Negative gearing works in your favour

If your property costs more to run than it earns in rent — which is common in the early years — that loss can be deducted directly against your personal income. Your salary, your business income, whatever else you earn. It reduces your taxable income for the year and cuts your tax bill accordingly.

A company can’t do this for you. Any loss the company makes stays inside the company. It doesn’t flow through to reduce what you personally owe the ATO. For investors counting on the negative gearing benefit as part of their strategy, this is a meaningful gap.

Setup is simple and ongoing costs are low

There’s no extra paperwork, no registering anything with the government, no separate bank accounts to maintain or corporate filings to worry about each year. You buy property in Australia, a tenant moves in, and come tax time your accountant does what they always do. It fits into your existing life without adding a new layer of complexity on top of it.

Land tax thresholds tend to be more generous

In most Australian states, individuals enjoy a higher land tax-free threshold than companies. If you’re holding property across multiple assets, this adds up over time and keeps your annual holding costs lower.

Buying Under a Company — When It Makes Sense?

Company ownership isn’t for everyone — but for the right investor in the right situation, it offers some real advantages worth understanding.

Asset protection is the strongest argument

A company is its own separate legal entity. What that means in practice is that if you’re personally sued — for something unrelated to the property — your assets held inside a properly structured company are generally shielded from that claim. Your personal finances and your company’s assets sit in different buckets.

For business owners, professionals in high-liability industries, or anyone with significant personal exposure, this separation can be genuinely valuable. It’s not bulletproof and it depends heavily on how the structure is set up, but it’s a real layer of protection that personal ownership doesn’t offer.

The corporate tax rate can work in your favour on income

Companies pay a flat rate of 25–30% on their taxable income, depending on size and structure. If you’re a high-income earner sitting on a 47% marginal rate, rental income taxed at 30% inside a company sounds attractive.

The catch — and it’s an important one — is getting that money back out of the company and into your hands. Dividends attract additional tax. The corporate structure creates efficiency on the way in but complexity on the way out.

Retaining profits inside the company

If you’re building a larger portfolio and planning to reinvest earnings rather than draw them as personal income, a company structure lets you retain profits at the lower corporate rate and deploy them back into new investments. For long-term portfolio builders who don’t need the cash personally right now, this can be an efficient way to grow.

The Honest Trade-offs — Company vs Personal Name

The CGT Difference: Company vs Personal Name

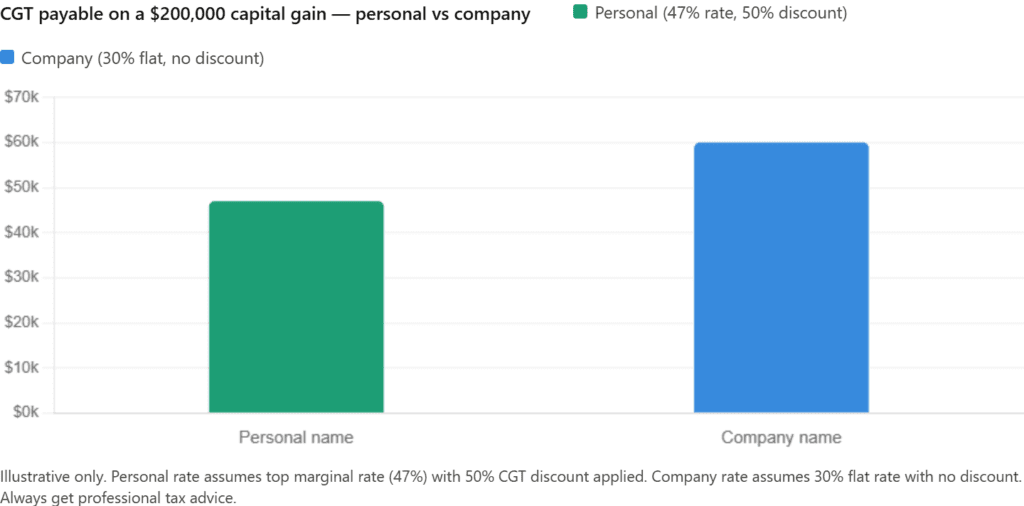

This is the one that surprises people most when they finally run the maths. Take a $200,000 capital gain on a property sold after more than 12 months.

- Personal name: The 50% CGT discount applies, so you’re taxed on $100,000. At the top marginal rate of 47%, that’s roughly $47,000 in tax.

- Company name: No CGT discount. With the full $200,000 at the 30% corporate rate. That’s $60,000 in tax.

- Same property: Same gain. Same holding period. $13,000 difference in tax — purely because of the ownership structure.

For investors who plan to hold and eventually sell, this is often the single most important number in the whole conversation.

Who does personal ownership actually suit?

Where you are in your investing journey matters more than most people realise when making this call.

For someone buying their first or second property, personal ownership usually makes the most sense — and not just because it’s simpler. The tax benefits are genuinely good. If the property runs at a loss in the early years, that loss works in your favour when your tax return comes around. And when you eventually sell after holding it for over a year, only half your capital gain gets taxed. That’s not a small thing — it’s one of the more generous concessions in the Australian tax system, and it’s only available to individuals.

On top of that, your life doesn’t get more complicated. No separate structure to maintain, no additional fees landing every year, no extra layer for your accountant to work through. For someone who wants to build wealth steadily without turning property into a part-time administrative job — personal ownership tends to be the one that fits without friction.

When does a company start to make sense?

It’s a different conversation for a different type of investor. If you’re running a business, work in a profession with real liability exposure, or you’ve already built up enough personal wealth that protecting it becomes a genuine priority — a company structure starts to earn its place.

The other scenario where it gets interesting is when you’re playing a longer game with a bigger portfolio.

And if you’re at the stage where you’re reinvesting earnings back into the portfolio rather than pulling them out as personal income, that changes the calculation too. The compliance costs that sound annoying at first start to feel more reasonable when the structure is actually doing something useful for you. A good accountant who knows your numbers — not a generic answer, but your specific situation — makes that call a lot clearer.

At the end of the day, one structure isn’t cleaner or smarter than the other across the board. They just suit different people at different stages of their investing life.

A Quick Summary: Company vs Personal Name

| Question | Short answer |

| What’s the most common choice? | Personal name — simpler and more tax-efficient for most |

| Who gets the 50% CGT discount? | Personal owners only — not companies |

| Can a company use negative gearing? | No — losses stay inside the company |

| What’s the company tax rate? | 25–30% flat, versus up to 47% personally |

| Is a company better for asset protection? | Yes — it’s the main reason to consider it |

| Is there a right answer for everyone? | No — get professional advice for your situation |

Which One You Will Choose: Company vs Personal Name?

This isn’t a decision to make casually or copy from someone else’s situation. The right structure depends on where you are financially, what you’re trying to build, and what risks you’re managing. For the majority of Australian investors — especially those starting out or building a modest portfolio — personal ownership is simpler, cheaper, and more tax-efficient. The 50% CGT discount and negative gearing benefits alone make a compelling case.

For investors at a different stage — with bigger portfolios, liability concerns, or a long-term reinvestment strategy — a company structure might earn its place. But it needs to be set up properly, maintained properly, and evaluated against your full financial picture.

The decision you make before you sign the contract is one of the few you can’t easily undo. Take the time to get it right. Thinking about your next property purchase and not sure which structure suits you? Get in touch with NextHouse — we’ll help you ask the right questions and find the right fit.

Disclaimer: This report is for educational and informational purposes only. It does not constitute financial, investment, or legal advice. Always seek professional advice before making property decisions.