Let’s cut straight to it. The Australian property market in 2026 is not in a straight line up. But it’s not falling off a cliff either. It’s doing something more complicated — and that’s exactly why the easy headlines keep getting it wrong. Here’s what the numbers are telling us right now:

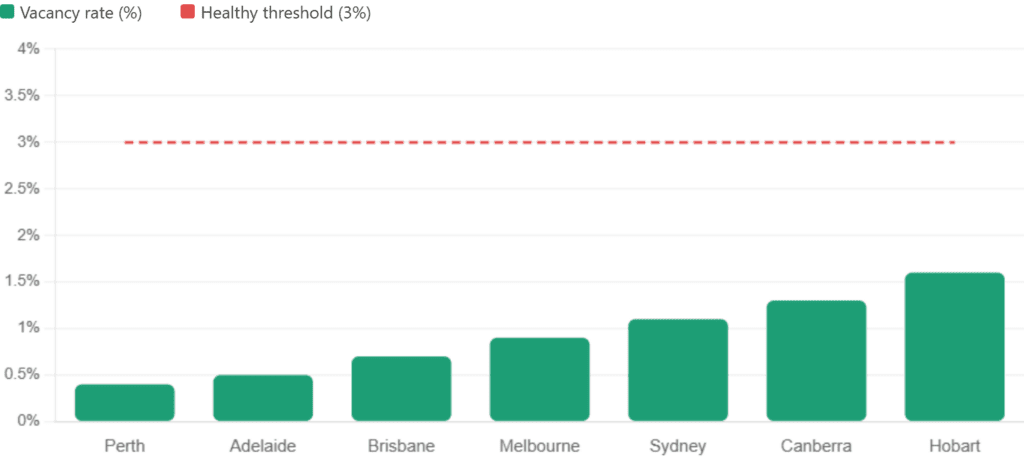

- National rental vacancy rates are sitting below 1% in most capitals — that’s extraordinarily tight

- New dwelling completions are still running way behind population growth

- Net overseas migration, while down slightly from 2023’s record, is still adding roughly 350,000 people a year to the country

Put those four things together and you get a market where demand is still outrunning supply — even as affordability is genuinely stretched.

Australian Property Market: Will Prices Crash in 2026?

This question is everywhere. And fair enough — prices have run hard over the past decade. But here’s the thing: a proper property crash needs specific ingredients. It needs either a sudden spike in forced sellers (like mass unemployment), or a flood of new supply hitting the market at once, or a credit crunch where banks stop lending. Right now, none of those three conditions are in place.

What you do have is:

| Condition | Where We Are |

| Unemployment | Sitting around 4.1% — low by historical standards |

| Housing completions | Running 30–40% below what’s needed |

| Bank lending standards | Tight post-APRA reforms, not reckless |

| Migration | Still 300,000+ net per year |

| Interest rates | Falling, not rising |

That doesn’t mean every market keeps going up. Melbourne has been the laggard in this cycle — slower growth, some suburbs flat or negative. Sydney has pockets of stress at the high end. But a national crash? The fundamentals don’t support it. And if you want a deep dive on what’s happening specifically in Melbourne right now, Ankur breaks it down here:

Watch YouTube: Melbourne Property Hit a 4-Year Low — Why the RBA’s May 5 Decision Changes Everything

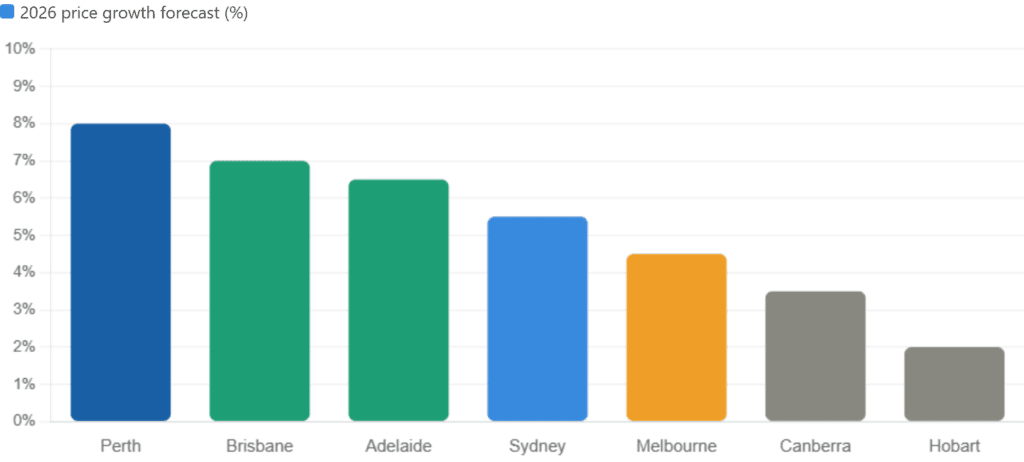

Australian property market forecast: City-by-City Breakdown

Perth is still the tightest market in the country. It ran 50%+ over three years and hasn’t stopped. Supply is genuinely constrained and the resource economy keeps wages high. ANZ’s forecasts suggest the boom is moderating — but it’s not reversing yet.

Brisbane is the one ANZ has been bullish on all year. The Olympics pipeline, interstate migration, and a genuine supply shortage have pushed Brisbane into genuine top-tier territory. The gap with Melbourne is closing fast.

Melbourne is the most interesting market right now — for all the wrong reasons. It’s been soft while every other capital ran. Land taxes, rising costs, and some genuine population softness post-COVID have weighed on it. But rate cuts, tight rentals, and cheap entry prices in the outer suburbs are setting up a potential recovery in late 2026.

| City | 2026 Price Forecast | Key Driver | Watch Out For |

| Perth | +7–9% | Undersupply, resource sector | Already run hard — watch entry price |

| Brisbane | +6–8% | Interstate migration, Olympics pipeline | Some suburbs overstretched |

| Adelaide | +6–7% | Affordability, interstate buyers | Limited stock but limited upside ceiling |

| Sydney | +4–6% | Lifestyle demand, income migrants | Affordability wall at the top end |

| Melbourne | +3–6% | Rate cuts, rental pressure | Slowest recovery, land tax headwinds |

| Canberra | +3–5% | Government employment stability | Slowdown in public sector hiring |

| Hobart | +2–4% | Lifestyle buyers cooling slightly | Weaker interstate demand |

The Rental Crisis Isn’t Going Anywhere

This is the part that most 2026 forecasts gloss over. And it’s arguably more important for understanding where prices go than the RBA cash rate.

Vacancies below 1% are not normal. A healthy rental market runs at around 2.5–3%. Below 1% means tenants are in fierce competition for every available property. That means:

- Rents keep rising (Melbourne rents are up 20–25% over three years)

- Renters are being squeezed toward ownership — even if they can barely afford it

- Investors who stayed in the market are getting strong yields for the first time in years

Here’s the brutal math on why the crisis isn’t ending soon:

| Factor | Direction |

| New apartment completions | Still well below demand |

| Short-term rental platforms (Airbnb) | Still removing stock from long-term pool |

| Investor selling (land tax, cost pressure) | Adding to rental scarcity |

| Migration | Adding rental demand faster than supply |

For a deep look at how 21,000 rental properties literally disappeared from Melbourne’s market in one year:

Regional Markets: Still Worth Watching

Regional Australia had its moment in 2020–2022 when remote work sent buyers searching for space. That boom has mostly cooled. But some regional markets are still performing quietly well. The ones worth watching in 2026:

| Region | Why It’s Interesting |

| Geelong, VIC | Melbourne overflow, infrastructure investment |

| Sunshine Coast, QLD | Lifestyle + strong migration |

| Newcastle & Central Coast, NSW | Sydney overflow, relative affordability |

| Ballarat & Bendigo, VIC | State government investment, cheaper entry |

| Townsville, QLD | Resources sector, lower vacancy rates |

Should You Buy, Hold, or Wait?

This is the question everyone actually wants answered. And honestly, it depends on who you are.

- If you’re an investor: The rental yield story is stronger than it’s been in a decade. Vacancy rates below 1% mean you’re unlikely to be without a tenant. But entry prices aren’t cheap — do the numbers properly on cashflow, not just capital growth assumptions.

- If you’re a first home buyer: Rate cuts have improved your borrowing power slightly. Government schemes (like Help to Buy, if it passes) could change the equation more. But affordability is still brutal in Sydney and Melbourne. The outer suburbs and regional cities are where first buyers are finding the numbers that actually work.

- If you’re deciding to hold or sell: For existing owners, 2026 is likely not a crisis year — but it’s not a boom year either for most markets. If you’re holding an investment property in Victoria and watching land tax eat your returns, the calculation is different.

And if you’re wondering how the federal budget’s changes to CGT and negative gearing affect all of this:

NextHouse View

The mainstream 2026 forecasts tend to either scare you or reassure you. Neither is that useful. Here’s what we actually think: The market is not going to crash. The structural drivers — migration, under-building, tight rentals — are too strong. Even if sentiment dips, the underlying demand is real.

But “the market” is a fiction. Perth and Melbourne are not the same story. A house in Tarneit and a unit on St Kilda Road are not the same investment. The averages hide more than they reveal.

Rate cuts matter, but not as much as the headlines suggest. A 0.25% cut doesn’t suddenly make a $900K Sydney mortgage affordable. The affordability wall is structural — you need either wages to grow faster, or prices to fall, or both.

The risk that nobody is talking about is the two-speed split within cities. Cheap outer suburbs absorbing migration demand and performing well. Expensive inner-ring markets — especially Victoria units — still struggling with supply, land tax, and cost pressures.

The smart move in 2026 is specificity. Stop thinking about “the market” and start thinking about specific corridors, specific infrastructure pipelines, specific vacancy rates. That’s where the real calls are.

Watch: 214,700 Aussie Investors Just Hit APRA’s New 6× Wall

People Also Ask

Will Australian property prices drop in 2026? A broad national drop looks unlikely given the supply shortage and rate cuts. But specific markets — particularly oversupplied unit markets in Melbourne and some regional towns — could see flat or negative movement.

Is now a good time to invest in Australian property? Rental yields are the strongest they’ve been in years, and vacancy rates are at historic lows. That’s a reasonable environment for investors. But entry prices are high and cost pressures (interest, land tax, maintenance) are real. Run the actual numbers — don’t just bet on growth.

Which Australian city will grow the most in 2026? Perth and Brisbane are the consensus picks from most major bank forecasts, including ANZ. Both have undersupply, strong migration, and relative (if now narrowing) affordability compared to Sydney.

How does the rental crisis affect property prices? Tight rentals push would-be renters into buying — increasing demand. They also support investor returns, keeping more investors in the market. Both effects put upward pressure on prices.

FAQs

- Is a property bubble going to burst in Australia?

The ingredients for a classic bubble burst — mass oversupply, reckless lending, sudden demand collapse — aren’t present right now. What you have instead is a market with stretched affordability that’s growing more slowly. A soft plateau in some markets is possible. A dramatic crash needs a trigger that isn’t visible yet. - What suburbs in Melbourne will perform best in 2026?

Outer growth corridors with infrastructure investment and genuine rental demand are the ones to watch — places like Werribee, Tarneit, and parts of the south-east. Inner-ring units are still facing headwinds. We’ve covered specific suburbs in detail on the NextHouse YouTube channel. - How will RBA rate cuts affect property in 2026?

Each 0.25% cut adds roughly $15,000–$20,000 to average borrowing capacity. That’s meaningful but not transformative. The bigger effect is psychological — rate cuts shift sentiment, and sentiment moves markets quickly. - Will the CGT changes affect property investors in 2026?

Yes, and this one’s bigger than most people realise. The proposed shift from a 50% CGT discount to a flat 25% rate changes the after-tax return calculation for long-term holders significantly. We’ve done a full breakdown on YouTube.

Related Reading

- Melbourne vs Brisbane: The $500K Reversal ANZ Predicts

- Perth Property 2026: Where Does the Boom Actually End?

- Melbourne Rental Crisis: Why 21,000 Properties Vanished

- CGT Reform 2026: What Every Investor Needs to Know

- Werribee and Tarneit: The Real Investment Case

References

- RBA cash rate decisions and meeting minutes, 2024–2025

- ANZ Research: Australian Housing Outlook 2026

- ABS Housing Finance, Building Approvals, and CPI data

- Domain and PropTrack median price and vacancy data

- NextHouse independent analysis — NextHouse.com.au

Disclaimer: This article is general information only and doesn’t constitute financial, investment, or legal advice. Every property market is different and every person’s situation is different too. Always talk to a licensed financial adviser or property professional before making any investment decision. NextHouse is an independent analysis platform — no buyer’s agency, no developer relationships, no financial products to sell. All data is sourced from publicly available research.