If you’ve been watching the Australian property market lately, you already know what it feels like to compete for yields in a market where prices never really pull back. So it makes sense that more Aussie investors are quietly turning their attention west — to the U.S. The 2026 American rental market tells an interesting story. Prices have levelled off in most cities, but tenant demand hasn’t. That gap — where demand outruns supply — is where a well-placed rental property makes serious money.

This guide breaks it all down. No fluff. Just the cities worth looking at, the numbers, and the honest tradeoffs.

Quick note for Australian readers: U.S. rental yields are generally quoted gross. Net yields — after property taxes, management fees, insurance, and maintenance — typically run 1.5–2.5% lower. All AUD/USD comparisons in this guide use an approximate rate of 0.65. Always get independent tax and legal advice before investing overseas.

What actually makes a city worth investing in?

This isn’t a mystery. The best rental markets share a few clear traits — and once you know what to look for, the shortlist writes itself.

A growing population means more renters. Affordable purchase prices mean better cash flow from day one. A diverse job market means the city isn’t one bad quarter away from a vacancy crisis. And landlord-friendly laws mean fewer regulatory headaches from the other side of the planet.

With those filters in mind, here’s what the data says for 2026.

The cities worth putting on your radar: Rental Property

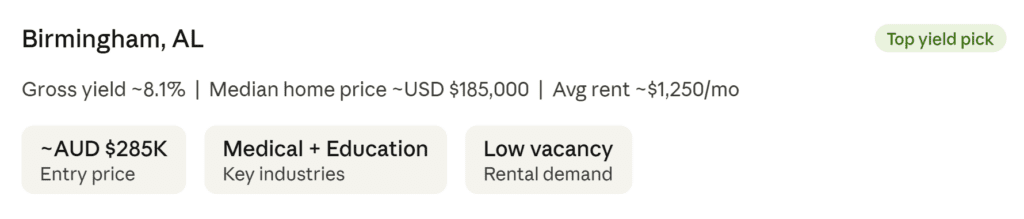

Birmingham, Alabama — the quiet outperformer

Birmingham doesn’t have the profile of a Dallas or a Phoenix. But for yield-focused investors, that’s kind of the point. Property prices here are still well below the national average, while rents have been remarkably stable over the past three years.

The local economy runs on healthcare, manufacturing, and education — three sectors that tend to hold up even when the broader market wobbles. And there’s genuine renewal happening in some inner suburbs, which adds a layer of capital growth potential most people aren’t pricing in yet.

Beaumont and Brownsville, Texas — small cities, real returns

Texas gets most of its press for Austin and Houston, but the smaller cities are quietly putting up better numbers on a yield basis. Beaumont runs on energy and port-related industries. Brownsville benefits from its position on the U.S.–Mexico border — trade, logistics, and manufacturing keep the local workforce steady.

These aren’t growth-story markets. They’re cash-flow markets. And for an Aussie investor who wants income rather than speculation, that’s not a bad thing at all.

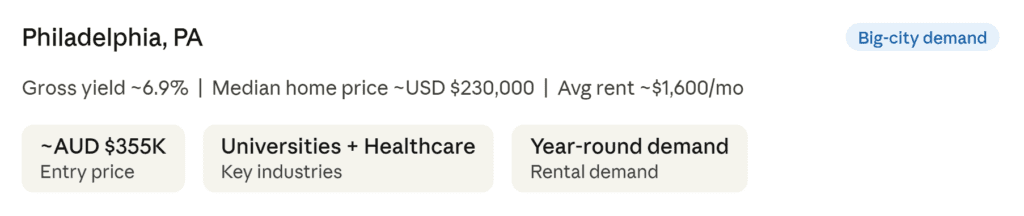

Philadelphia — big city demand, without the big city price tag

Philadelphia is what a lot of investors wish Sydney were: a genuine major city with a large, diverse rental market — but with prices that don’t require a seven-figure commitment to get started.

It’s home to one of the largest university populations in the U.S., a massive healthcare workforce, and a steady stream of young professionals who, for the most part, prefer renting to buying. The neighbourhood diversity also means you can calibrate your strategy — high yield in transitional areas, or stability and lower vacancy in established suburbs.

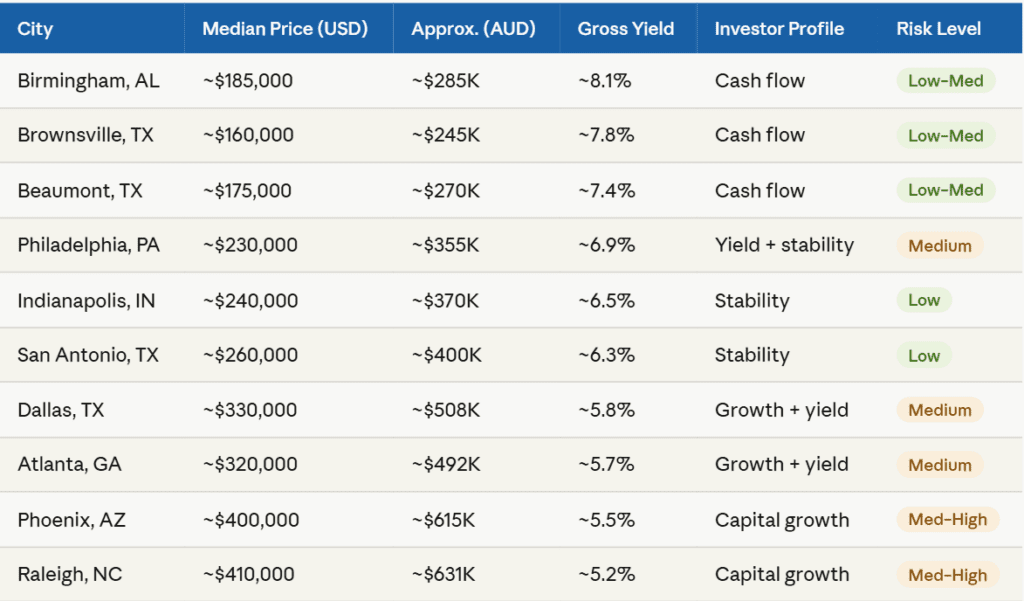

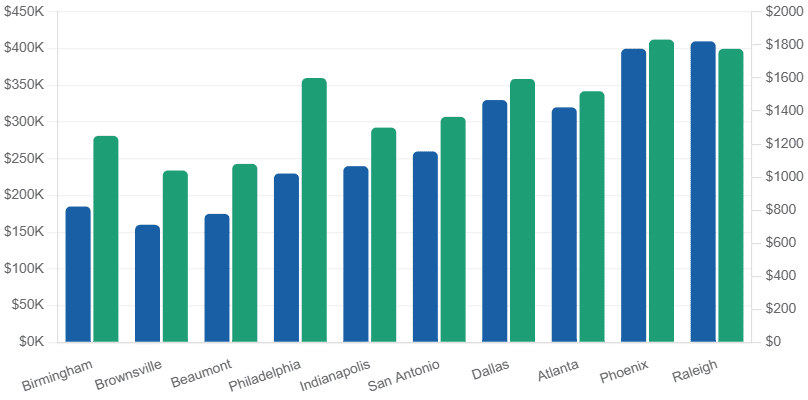

How do these markets stack up? The full comparison

Here’s a side-by-side look at the key metrics across every city covered in this guide. Use this as a starting point — not a final answer.

The growth plays: Dallas, Phoenix, Atlanta, Raleigh

These four cities aren’t the highest-yield options on the list. But they’re not trying to be. What they offer instead is a balance between steady rental income now and genuine capital growth over time.

Dallas has one of the most diversified economies in the U.S. — tech, finance, logistics, energy. It’s not a one-trick pony, which means it tends to hold up when things get choppy nationally. Phoenix and Atlanta both benefit from strong interstate migration. People are still moving there, and that keeps vacancy rates in check. Raleigh is smaller but punches above its weight — the Research Triangle drives a well-educated, well-paid tenant base that’s stable and long-term.

The reliable earners: Indianapolis and San Antonio

If your goal is quiet, consistent performance — the kind that doesn’t keep you up at night — Indianapolis and San Antonio deserve serious attention. Neither is flashy. But both have growing populations, broad employment bases, and housing markets that remain genuinely affordable by U.S. standards.

Vacancy rates in both cities have been well-controlled. Property management costs tend to be lower than in coastal markets. And the regulatory environment for landlords is reasonable. These are markets built for the long hold.

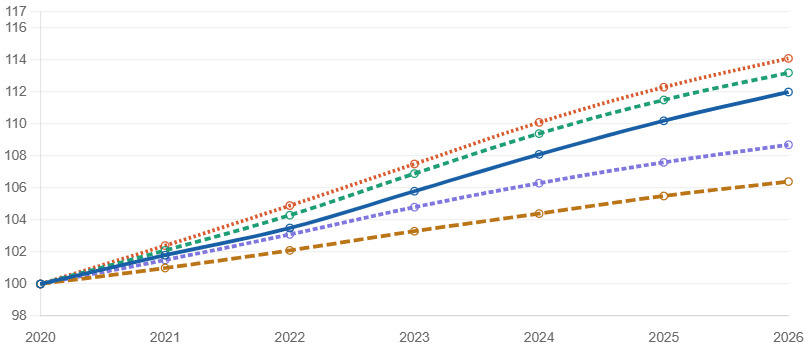

Population growth trend — selected U.S. cities 2020–2026 (index: 2020 = 100)

Also Watch: The Melbourne Boom Corridor Has a Crime Trajectory Nobody’s Tracking

What Aussie investors specifically need to know?

Investing across the Pacific comes with a few wrinkles that don’t apply when you’re buying in Melbourne or Brisbane. Here’s what to have sorted before you move.

First, currency. The AUD/USD rate matters more than most people account for. A 10% swing in the exchange rate can eat into or add to your returns significantly — and it cuts both ways. Build a buffer, or look at hedging options.

Second, structure. Most Australian investors buying U.S. property use an LLC (Limited Liability Company) to hold the asset. This gives liability protection and can simplify management, but it has tax implications on both ends. Get a U.S.-registered accountant who works with Australian clients — they exist, and they’re worth the cost.

Third, financing. U.S. banks will generally not lend to non-residents without a track record. Many Aussie investors either buy cash or use equity from Australian property to fund the purchase. Foreign national loans do exist but typically require 30–40% down and carry higher rates.

FAQs

- Can Australians legally buy property in the U.S.?

Yes. There are no restrictions on foreign nationals purchasing U.S. real estate. You’ll need a U.S. Individual Taxpayer Identification Number (ITIN) and should get specialist legal and tax advice on structure before buying. - Do I need to pay tax in both Australia and the U.S.?

Potentially, yes. Australia taxes its residents on worldwide income, so U.S. rental income is assessable here. The U.S.–Australia tax treaty helps avoid double taxation, but you’ll need to lodge returns in both countries. FIRPTA withholding applies when you sell. - What’s a realistic net yield after all costs?

Gross yields of 6–8% typically translate to net yields of 4–5.5% once you account for property taxes (1–2.5% of value annually), management fees (8–12% of rent), insurance, and maintenance. Still significantly higher than most Australian capital city yields. - Do I need to visit in person to buy?

Not necessarily. Many transactions are completed remotely with the right team in place — a local buyer’s agent, property manager, and attorney. That said, at least one visit before purchasing in a new market is strongly recommended. - What’s the minimum I need to invest?

In markets like Birmingham or Brownsville, entry-level investment properties start around USD $120,000–$180,000 (roughly AUD $185,000–$277,000). That’s a fraction of what a comparable investment property costs in Sydney or Melbourne. - Which city is best for a first-time overseas investor?

Indianapolis and San Antonio are often recommended for first-timers — stable, predictable, and forgiving. Birmingham offers better yields but requires slightly more local market knowledge to navigate well.

The NextHouse View

The U.S. rental market in 2026 presents a genuine opportunity for Australian investors who are priced out of domestic yield plays. The cities in this guide aren’t random picks — they’re markets with real fundamentals: population growth, job diversity, and landlord-friendly conditions. That said, this is not a simple market to navigate remotely. Currency risk, tax complexity, and financing constraints are real. Our view is that the best approach is to start small, build local networks, and treat the first purchase as a learning investment, not a retirement plan. The opportunity is real. So is the homework required to do it properly.

Disclaimer: This article is produced by NextHouse.com.au for general informational purposes only. It does not constitute financial, investment, tax, or legal advice. All yield figures and price estimates are approximations based on publicly available market data and are subject to change. Currency conversions are indicative only. Australian investors should seek independent financial and tax advice before making any investment decision. Past market performance is not a reliable indicator of future returns. NextHouse does not receive commissions from any U.S. property sales or referrals mentioned in this article.