If you’ve ever thought about dipping into the U.S. property market — whether it’s a vacation rental in Florida, a cash-flow play in the Midwest, or a long-term hold in a growing Sun Belt city — there’s one thing that can quietly eat into your returns if you ignore it early: property taxes.

And no, they don’t work like Australia. Not even close. Back home, we deal with stamp duty upfront and land tax annually. In the U.S., property tax is charged every single year based on your property’s assessed value — and the rate varies wildly depending on which state, county, or even municipality your property sits in. Two houses with the same price tag in two different U.S. states can have annual property tax bills that differ by thousands of dollars.

So if you’re doing the numbers on a U.S. deal, the tax rate you’re paying year after year matters just as much as the purchase price. Let’s break it down simply.

How U.S. Property Tax Actually Works?

In Australia, we pay stamp duty once when we buy, and then land tax each year on investment properties above a certain threshold. The federal government doesn’t touch that — it’s a state thing.

In the U.S., it’s similar in one way: there’s no federal property tax. It’s all handled at the state, county, and sometimes city level. What this means is that two suburbs in the same metro area can have completely different tax rates — and that’s before you factor in local school levies, special assessments, or exemptions.

The number investors track is called the effective property tax rate — that’s the actual percentage of your property’s value you pay in tax each year. It’s not always the same as the “nominal” rate on paper, because assessed values can differ from market values.

Think of it like this: if you own a property worth USD $400,000 and the effective rate is 0.5%, you’re paying $2,000 a year. If the effective rate is 2.5%, you’re paying $10,000 a year on the exact same asset. That’s the difference between a well-performing rental and a barely-breaking-even headache.

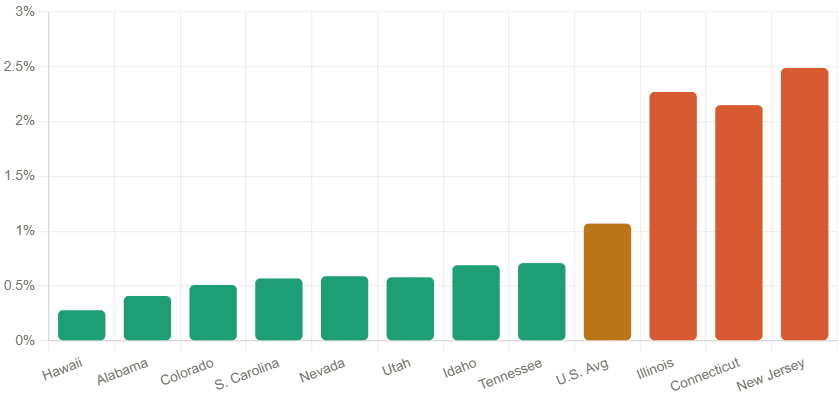

Effective Property Tax Rates by State

Effective annual rate as % of property value. U.S. national average = 1.07%.

The Low-Tax States Worth Watching

Here are the states that consistently come out on top for tax efficiency — and what that actually means in plain terms.

Hawaii — Surprisingly Tax-Friendly

Hawaii gets a bad reputation for being expensive, and yes, property prices there are among the highest in the country. But the effective property tax rate is typically below 0.30% — one of the lowest in the entire U.S.

If you’re considering a vacation rental or a long-term hold in Hawaii, the tax bill won’t hurt you the way it might elsewhere. The bigger challenge is the purchase price itself and the competition in the market.

Alabama — Low Prices, Low Taxes

Alabama is the kind of market that rarely makes headlines, which is exactly why it’s worth paying attention to. Property prices are modest by U.S. standards, and property tax rates are equally low. Homestead exemptions (similar in concept to owner-occupier concessions in Australia) reduce annual bills further.

For investors chasing cash flow — steady rental income with manageable costs — Alabama is worth a serious look.

Colorado and Nevada — Balance Done Right

Neither state is cheap anymore (especially Colorado, where Denver has been booming), but their effective property tax rates remain well below the national average. You get liveable cities, solid rental demand, and reasonable ongoing holding costs.

Nevada also has no state income tax, which adds another layer of appeal for investors thinking about the full tax picture.

South Carolina and Utah — The Overlooked Pair

These two states are starting to appear more on investors’ radars, and for good reason. Both have growing populations, improving infrastructure, and property tax environments that don’t punish landlords. South Carolina in particular has seen strong interstate migration from high-cost northeastern states — which is good news for rental demand.

Other States Worth Noting: Idaho, Delaware, Tennessee

All three sit comfortably below the U.S. national average in terms of effective property tax rates. Tennessee also has no state income tax, making it a double benefit for investors tracking net returns.

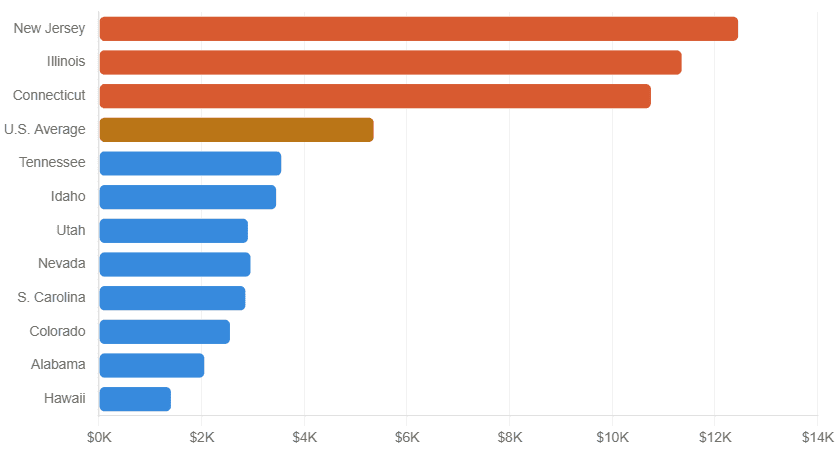

State-by-State Comparison for Australian Investors

Estimated annual tax bill in USD on a $500,000 property across U.S. states.

The States to Watch Carefully

This isn’t a warning to never buy in these states — good deals exist everywhere. But New Jersey, Illinois, and Connecticut are consistently ranked as the highest property tax states in the U.S., with effective rates sitting between 2% and 2.5% annually. To put that in context: a $500,000 property in New Jersey could cost you $10,000 to $12,000 in property tax alone every year. In Hawaii or Alabama, the same asset might cost you $1,500 to $2,000.

That gap doesn’t make high-tax states a no-go — strong job markets, quality schools, and high rental demand can more than compensate — but it means your spreadsheet needs to account for it properly before you fall in love with a deal.

Annual Property Tax Cost on a USD $500,000 Property by State

How This Stacks Up Against Australia

Here’s a question we get a lot from Australian investors: “Is U.S. property tax worse than what we pay at home?”

Short answer: it depends on the state, but for many U.S. states — especially the low-tax ones — it can actually be more manageable than what investors pay in land tax in Victoria or New South Wales once their portfolio grows.

In Victoria, land tax is applied on the unimproved value of investment properties, and the thresholds and rates have tightened considerably in recent years. Once you hold multiple properties, the land tax bill in Victoria alone can be significant.

In a U.S. state like Alabama or South Carolina, your property tax bill is predictable, relatively flat, and often lower as a percentage of value than Australian land tax for portfolio investors.

That said — don’t forget that owning U.S. property as an Australian also brings in considerations around U.S. federal tax on rental income, capital gains treatment, and potential estate planning complications. These are separate from state property tax, and they’re a conversation for a qualified international tax adviser.

Australia vs U.S. Property Tax System Comparison

| Factor | Australia | United States |

| Who sets the rate? | State government | State, county, or local govt |

| Upfront purchase tax? | Stamp duty (often 4–6%) | No equivalent (transfer tax, much smaller) |

| Annual holding tax? | Land tax on investment properties | Property tax on all owners (incl. owners-occupiers) |

| Based on what value? | Unimproved land value | Assessed property value (land + building) |

| Portfolio investors | Land tax compounds across multiple holdings | Each property taxed separately at local rate |

| Rate range (typical) | 0.5% – 2.5% land tax (Vic, NSW) | 0.28% – 2.49% by state |

| Federal property tax? | No | No |

| Who pays? | Investors only (above thresholds) | All property owners, every year |

What Should You Actually Do With This Information?

Here’s the NextHouse take: property tax efficiency should be on your checklist, not your headline.

It’s one variable in a bigger equation. You still need to evaluate:

- Rental yield — Is the market actually generating income at a rate that works post-tax?

- Capital growth potential — Is the population growing? Is the economy diversified?

- Liquidity — Can you sell when you need to?

- Currency risk — AUD/USD movement affects your real returns

- Management costs — U.S. property management fees can differ significantly by market

A low tax rate in a stagnant market is not a win. A slightly higher tax rate in a growing city with strong rental demand can still deliver excellent returns.

Do the full numbers. That’s what separates a smart investor from someone who got excited about a low rate.

NextHouse View

At NextHouse, we’re not here to push you toward a particular market. We don’t take commissions, we don’t have partnerships with U.S. developers, and we don’t have a financial product to sell you.

What we do is cut through the noise and give you a cleaner picture of how these markets actually work — so that when you’re sitting across the table from a U.S. buyer’s agent or scrolling through listings on Zillow at midnight, you’ve already got the right questions ready.

U.S. property can be a legitimate part of a diversified portfolio. But it rewards the investor who does the homework — and property tax efficiency is one part of that homework that most people skip.

Disclaimer: This article is for general information only. Tax laws change, and every investor’s situation is different. Please speak to a qualified tax adviser or buyer’s agent familiar with U.S. property before making any decisions. NextHouse does not provide financial or tax advice.