If you’ve been thinking about where to park your hard-earned capital in 2026, you’re not alone. Property is one of the most discussed fields of investment, and it has a right to be so: it is a tangible asset, may generate income, and can be a good long-term wealth-generating activity.

However, there are numerous markets all around the world; which one do you choose? This is the breakdown of the real estate investment story of Australia, Dubai and the USA in this guide, and it will help you calculate which one may provide the best ROI (return on investment) this year.

First, Let’s Get the Numbers on the Table

Before we get into the storytelling, here’s what the data actually looks like across the three markets right now.

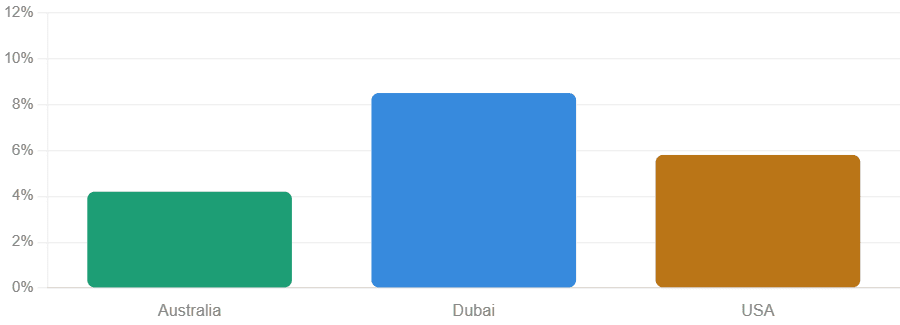

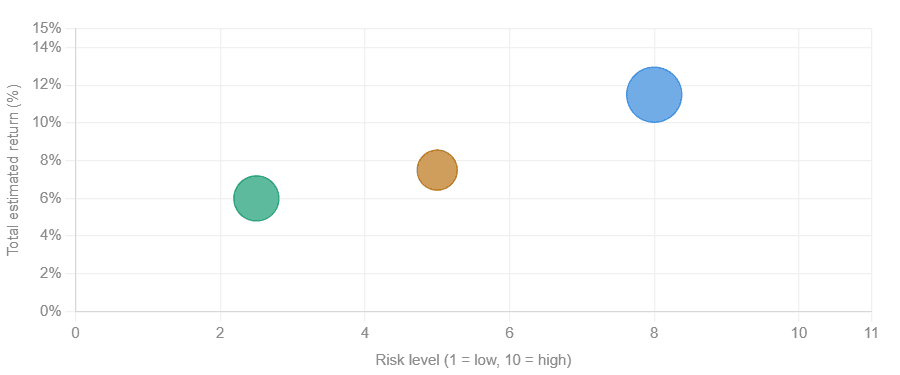

- Australia gross rental yield: ~4.2% | Projected capital growth 2026: 7.7%

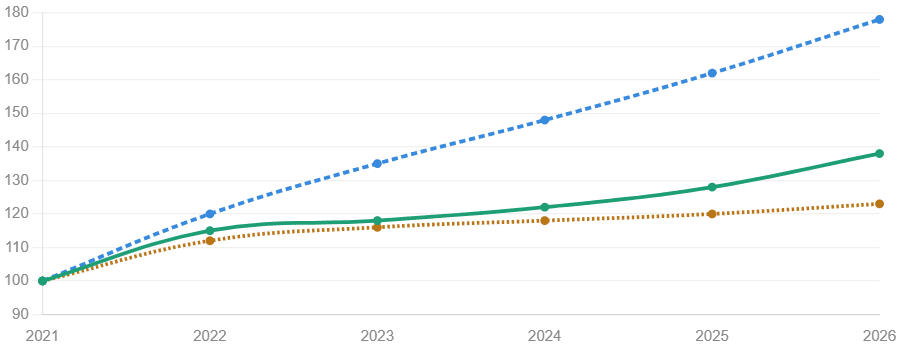

- Dubai gross rental yield: ~8–10% | Capital growth (5yr index): ~78% since 2021

- USA gross rental yield: ~5.8% | Capital growth 2026: Modest 1–3% nationally

Watch: 1 in 3 Melbourne House Sales Now Goes to Indian Buyers — The Data Reshaping Every Suburb

Market Comparison at a Glance

Every market has its own personality. Australia plays the long game. Dubai chases the yield. The US offers a scale you can’t find anywhere else. Before we dig into the details, here’s how they stack up side by side — so you’ve got the full picture before we break each one down.

Australia: Boring in the Best Way Possible

Let’s start at home.

The Australian property market doesn’t make headlines for overnight millionaires. It makes headlines for consistent, decade-on-decade wealth creation — and that’s actually the whole point.

In 2026, national house prices are forecast to grow by roughly 7.7%. Units are also ticking up, driven by persistent demand and a supply pipeline that just can’t keep up with population growth. Australia’s net overseas migration is still running hot, especially in Sydney, Melbourne, and Brisbane — and someone needs to live somewhere.

Rental vacancy rates in major capitals are sitting at historical lows. That means landlords have pricing power. Yields in inner-ring suburbs might look lower on paper (3.5–5%), but capital growth tends to make up the gap over time.

What Australians also have on their side is regulatory certainty. You know the rules. You understand the legal system. You can see the planning maps. There’s no currency conversion risk and no foreign ownership headaches.

Who’s it for? Investors who want steady compounding growth, manageable risk, and don’t need a flashy ROI story to sleep at night.

The honest downside? Entry prices are high. Stamp duty hurts. Negative gearing helps — but only if you’re in the right tax bracket. And if you’re buying in a major capital, you’re competing hard.

Dubai: The ROI Rockstar (With a Few Asterisks)

Dubai is impossible to ignore if you’re chasing yield. We’re talking 8–10% gross rental returns — more than double what you’d typically see in Sydney or Melbourne.

And that’s before you factor in the tax picture.

In Dubai, there’s no income tax on rental earnings. No capital gains tax either. For an Australian investor used to handing 30–45% of rental income back to the ATO, that’s a significant difference in net returns. The maths can look very compelling very quickly.

The off-plan payment structure is another drawcard. Developers in Dubai often allow staged payments during construction — meaning you can control a $500,000 property with a much smaller upfront commitment. That kind of leverage amplifies returns.

And then there’s the Golden Visa angle. Buy a qualifying property above a set threshold and you can access long-term UAE residency. That’s a financial and lifestyle play rolled into one.

But here’s what the brochure doesn’t always say:

Dubai’s market is more volatile. Prices can swing harder and faster than in mature markets. The 2009 crash wiped significant value — and while the market has matured since, volatility is still part of the deal. You’re also dealing with currency exposure (AED to AUD), a different legal system, and asset management from the other side of the world.

Who’s it for? Investors who understand the risk, want short-to-medium term income maximisation, and have the stomach for a market that can move sharply in either direction.

USA: Scale, Depth, and Diversity

The American market is enormous — and that’s both its strength and its complexity.

Nationally, US house prices are forecast to grow modestly in 2026. Maybe 1–3%. That’s not a headline-grabbing number. But zoom in and the picture changes. Certain Sun Belt cities — think Austin, Phoenix, Nashville — have been outperforming significantly. And multifamily (apartment) real estate in the right locations is generating 5–7% gross yields with relatively stable tenancy.

The US also offers something neither Australia nor Dubai can match at the same scale: liquidity through REITs. If you don’t want the hassle of direct ownership, you can get diversified US property exposure through listed real estate investment trusts — some with dividend yields of 5–8%.

Commercial real estate — particularly industrial and data centres — is also doing well in the US, riding e-commerce and AI infrastructure demand.

The catch? The US tax system is complex for foreign investors. Withholding tax applies. State-level taxes vary enormously. And property management across 14,000 kilometres is genuinely difficult without a trusted local partner.

Who’s it for? Investors who want diversification, structural depth, and the option of passive exposure through REITs rather than direct ownership.

The Real Comparison: After-Tax Returns

This is where the conversation gets interesting for Australians.

| Market | Gross Yield | Tax Impact (AUS investor) | Est. Net Yield |

| Australia (Sydney/Melb) | 3.5–5% | Marginal rate (32.5%–47%) + CGT | 2–3.5% net |

| Dubai | 8–10% | No local tax | 7–9% net* |

| USA | 5–7% | US withholding + AUS tax credit | 3–5% net* |

Estimates. Always get independent tax advice for your specific situation.

The point isn’t that Dubai is “better.” The point is that gross yields alone don’t tell the full story. Once you factor in taxes, management costs, currency risk, and entry/exit friction — the gap narrows. But for certain investor profiles, it narrows differently.

5 Questions to Ask Before You Invest Overseas

Before you wire money to any offshore property, run through these honestly:

- What’s your actual investment horizon? Dubai rewards short-to-medium plays. Australia rewards patience. The US depends on your asset class.

- Can you manage this remotely? An empty apartment in Dubai with a bad property manager can eat your yield fast.

- Have you stress-tested the currency? AUD/AED and AUD/USD fluctuation can wipe several percentage points of return if timing is wrong.

- Do you understand the local tax rules — and how they interact with Australian tax? Australia taxes its residents on worldwide income. Foreign tax credits exist, but the rules are complex.

- Is your capital tied up or liquid? Selling in some markets takes months. Make sure you don’t need the cash quickly.

The NextHouse View

At NextHouse, we’re not here to tell you where to invest. We’re here to make sure you’re making decisions on real data — not marketing spin.

Here’s what we’ve seen work for Australian investors:

- For most Australians, home-market investing still wins on a risk-adjusted basis. You know the rules. You understand the system. And the 7.7% projected growth for 2026 isn’t something to dismiss.

- For sophisticated investors with higher risk tolerance and offshore capability, Dubai’s tax-free yield story is genuinely compelling — but needs to be stress-tested properly.

- For passive exposure to the US market, REITs are worth exploring before committing to direct ownership.

The best ROI isn’t always the biggest number. It’s the one that fits your life, your tax position, and your plan.

FAQs

- Can Australians legally buy property in Dubai?

Yes. Dubai is one of the most open markets in the world for foreign property ownership. Certain designated freehold areas allow 100% foreign ownership. - Do Australians pay tax on income from overseas property?

Yes. The ATO taxes Australian residents on worldwide income. You may be eligible for foreign tax credits to offset what you’ve paid overseas, but you still need to declare it. - Is Dubai property a safe investment in 2026?

“Safe” is relative. Dubai has matured significantly as a market, but it carries more volatility than Australia. It suits investors who can absorb short-term fluctuations in exchange for higher yields. - What’s the minimum budget to invest in Dubai from Australia?

Off-plan properties can start from AUD $250,000–$350,000 equivalent in some areas. For established property in prime zones, you’re generally looking at AUD $500,000+. - Which market has the best capital growth potential right now?

Dubai has shown the strongest raw capital growth over the past 5 years. Australia’s growth is more consistent and less volatile. The US is modest at a national level, with pockets of strong performance. - Is negative gearing available for overseas properties?

Yes — Australian investors can negatively gear overseas properties. However, the rules are complex and the tax treatment of foreign losses has specific requirements. Get proper advice. - Should I use a buyers agent for overseas property?

For Dubai and the US — strongly recommended. The market dynamics, developer reputation checks, and local legal nuances are difficult to navigate from Australia without experienced local representation.

Disclaimer

This article is general information and does not constitute financial product advice, tax advice, mortgage broking advice, real estate advice or legal advice. It is not a recommendation to buy, hold or sell any asset, security or property. NextHouse is not licensed under an Australian Financial Services Licence (AFSL) or an Australian Credit Licence (ACL). NextHouse operates under the ASIC s.911A(2)(eb) information service exemption.

The reform is proposed — not yet legislated. The package requires passage through both houses of Parliament. The Coalition has indicated it will not support the CGT, negative gearing or trust changes. Always speak to a licensed financial adviser, registered tax agent and licensed mortgage broker (MFAA or FBAA member) about your specific situation before acting on any information in this article.

NextHouse does not accept paid placement from developers, agents, lenders or builders. No commercial relationship exists with any party referenced in this article.