Every time the world goes sideways — a war breaks out, markets tank, world crisis, China sneezes — your phone blows up with hot takes about what it means for Melbourne property.

Most of them are wrong. Not because the world doesn’t matter. It does. But because there’s a very specific chain of events that has to happen before a global crisis actually shows up on your street — and most crises don’t make it that far.

After 10 years tracking how global events move Melbourne suburbs, one pattern keeps coming up again and again. And once you see it, you can’t unsee it. Here’s the whole thing, laid out simply.

The Big Idea: One Value Does Almost All The Work

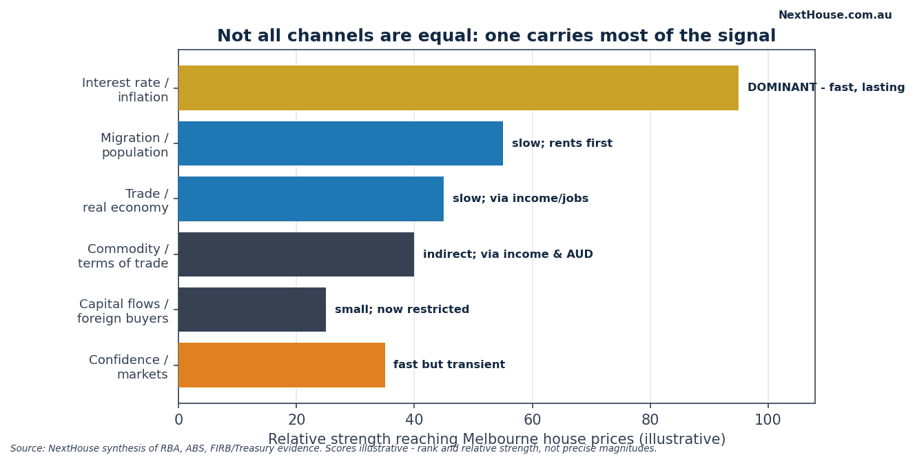

Any world event reaches Melbourne through six possible paths. But one of them — interest rates — carries about 80% of the force.

→ Will this move the RBA cash rate?

If yes, Melbourne feels it. If no, Melbourne mostly ignores it — however scary the headlines look. That’s the whole framework. But let’s walk through exactly how it works, so you can run it yourself next time.

The Big Four Number: Reaches Your Melbourne Suburb

Before we go any further, here are the four data points that underpin everything below.

| # | The number | What it means |

| 1 | ~1/3 | A permanent 1% rate rise lowers real house prices by roughly one-third over the long run (RBA Saunders-Tulip model) |

| 2 | ~4× | The same rate shock hits some suburbs four times harder than others (RBA RDP 2020-02) |

| 3 | <1% | Foreign buyers account for less than 1% of national property turnover — $4.9B vs ~$674B (FIRB / PEXA) |

| 4 | 80%+ | More than 80% of Australian mortgages are variable or short-fixed, so rate changes hit fast (RBA) |

That first number is the big one. A 1% permanent rate rise = roughly one-third off real house prices over time. That’s not a theory. That’s the RBA’s own housing model.

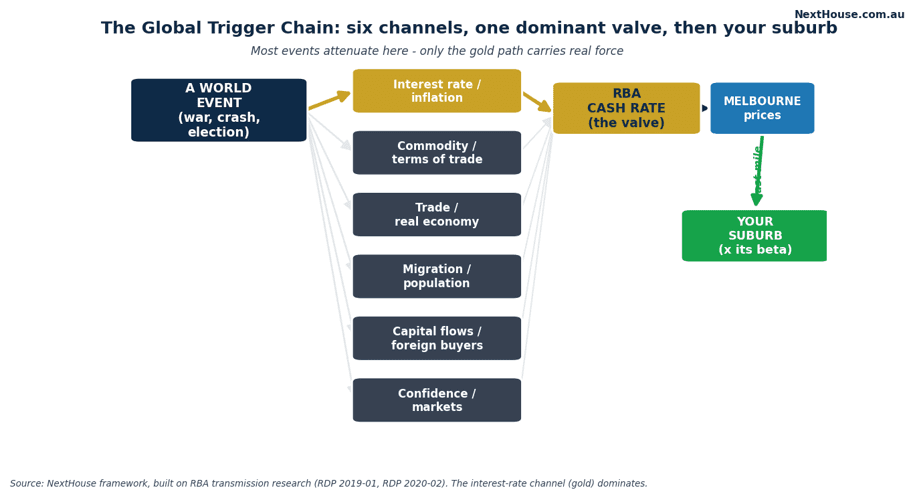

THE GLOBAL TRIGGER CHAIN

Here’s the whole picture in one place. A world event fans out into six possible paths. But only one — the interest-rate path — reliably carries real force all the way to your suburb.

And here’s that same picture as a scorecard you can use on any event:

| Channel | Strength for Melbourne housing | Speed | How long does it last? |

| Interest rate / inflation | STRONG — the dominant path | Fast | Lasting |

| Migration / population | Moderate — shows up in rents first | Slow | Structural |

| Trade / real economy | Moderate for income, weak for housing | Slow | Medium |

| Commodity / terms of trade | Weak-moderate, indirect | Slow | Diffuse |

| Capital flows / foreign buyers | Weak in total; now restricted | Medium | Suppressed |

| Confidence / financial markets | Weak-moderate — moves sentiment | Fast | Fades fast |

Source: NextHouse synthesis of RBA, ABS and FIRB/Treasury evidence.

THE SIX CHANNELS — HONESTLY RATED

Every global event reaches Melbourne through one or more of these six paths. The art of reading a crisis is knowing which one it travels down — and how much signal survives the trip.

Here’s a quick guide to which events travel which way:

| World event | Main channel(s) | Does it reach the cash rate? |

| US inflation surprise | Interest rate / inflation | Yes — directly |

| Oil / energy price shock | Commodity → inflation | Yes — it raises inflation |

| Pandemic | Confidence, then rates | Yes — via emergency cuts |

| China property slump | Commodity / trade | Only if it shifts AU inflation |

| A foreign election result | Confidence | Rarely |

| Global banking scare | Confidence / capital | Usually not — fades in weeks |

Source: NextHouse framework. The third column is the decisive test.

THE DOMINANT CHANNEL: INTEREST RATES

This is where the action is. When global inflation rises — say because oil prices spike or the US Fed hikes — the RBA eventually responds by adjusting Australia’s cash rate. That hits mortgage repayments almost immediately, because most loans are variable. That changes how much buyers can borrow. That changes what they can pay.

Fast, powerful, and durable. That’s why this channel does most of the work.

Two things make it unusually powerful in Australia specifically:

- Most mortgages are variable. The fixed-rate share peaked near 40% during COVID and has since fallen back hard, with most fixed loans repricing within two years. A cash-rate change reaches household budgets fast.

- Households are heavily geared. That’s high. It means rate moves bite harder here than in most other countries.

One more thing worth knowing: Australia doesn’t just blindly follow the US Fed. The RBA sets its own cash rate to domestic inflation and jobs. Through 2024–25 the Fed was cutting while the RBA held at 4.35%. In 2026 the RBA actually hiked on local inflation. The global event sets the backdrop. The RBA’s domestic mandate pulls the trigger.

That’s precisely why the right question is never “how big is this crisis?” — it’s “what will it do to the cash rate?”

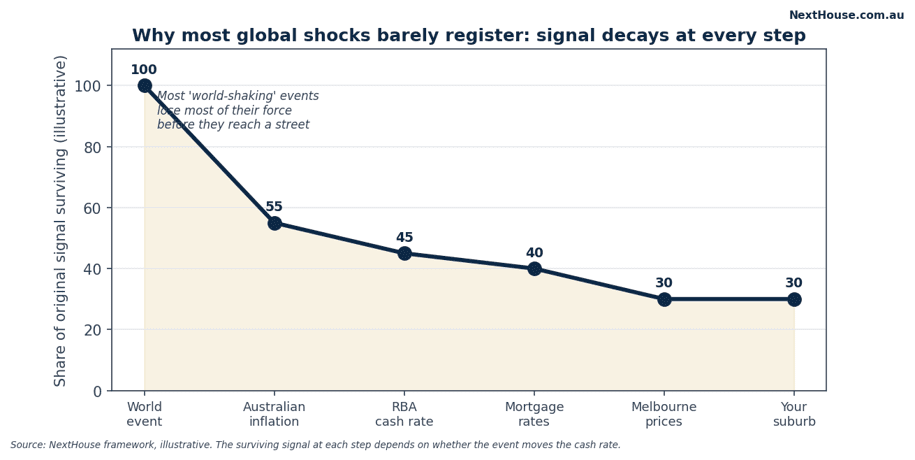

WHY MOST GLOBAL EVENTS DO NOTHING TO YOUR SUBURB?

Here’s the honest reason your suburb doesn’t feel most world events: heavy signal loss at every step.

A distant war, a foreign election, a far-off financial panic — each one has to first change Australian inflation, then change the cash rate, then change mortgage rates, then change borrowing capacity, before it touches a single Melbourne price. At every step, most of the force leaks away.

This is why the historical record looks so one-sided. The events that moved Melbourne — the GFC, COVID, the post-Ukraine inflation surge — all moved the cash rate. The events that didn’t change the rate path left almost no mark, however alarming the headlines were.

If you remember one thing from this: an event with no rate consequence is, for Melbourne property, mostly noise.

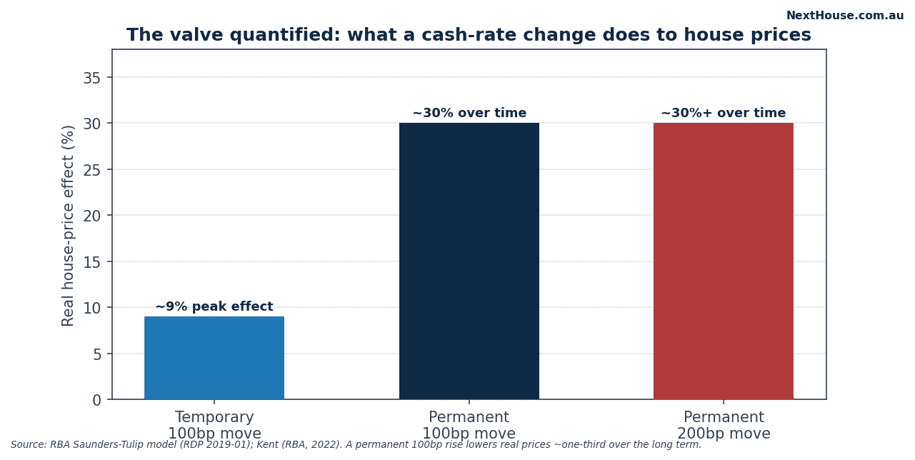

THE MASTER VALVE: WHAT A RATE CHANGE ACTUALLY DOES

The RBA’s own housing model (the Saunders-Tulip framework) gives us the clearest picture available:

| Rate change type | Estimated price impact |

| Permanent +1% rise | ~−33% real prices over the long run |

| Temporary +1% rise | ~−9% at peak, then unwinds |

Source: RBA Saunders-Tulip model (RDP 2019-01); Kent (RBA, 2022).

The crucial word is permanent. Markets respond to where rates are expected to settle — not just where they are today.

A rate move that lasts two years does far more damage (or good) than one that’s reversed in six months. So when you’re reading a crisis, don’t just ask “will this move rates?” Ask: will the move stick? That’s the difference between a scare and a structural shift.

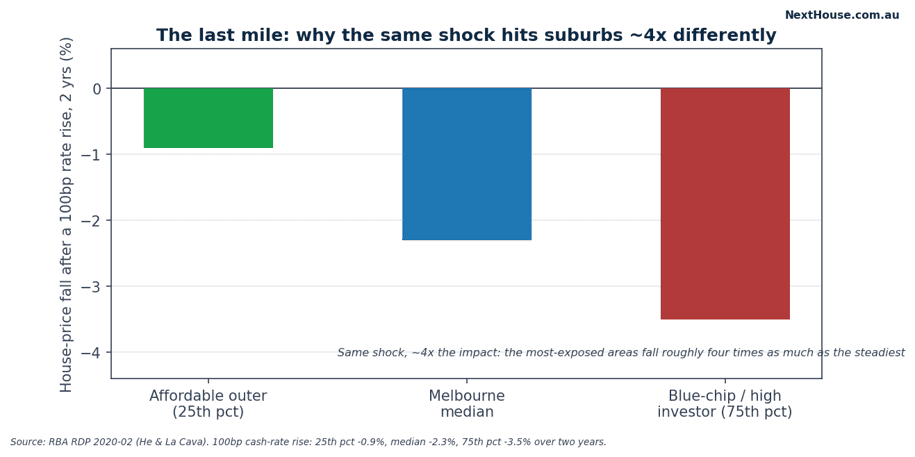

THE LAST MILE: WHY YOUR SUBURB ISN’T LIKE YOUR NEIGHBOUR’S

Here’s the step nobody talks about — and the most personal part of this whole framework.

A Melbourne-wide move doesn’t land evenly. RBA research shows the same rate shock hits the most exposed suburbs about four times harder than the steadiest ones.

| Sensitivity | Estimated price fall (100bp rate rise, 2-year view) |

| Most sheltered suburbs | ~−0.9% |

| Median suburb | ~−2.3% |

| Most exposed suburbs | ~−3.5% |

Source: RBA RDP 2020-02 (He & La Cava).

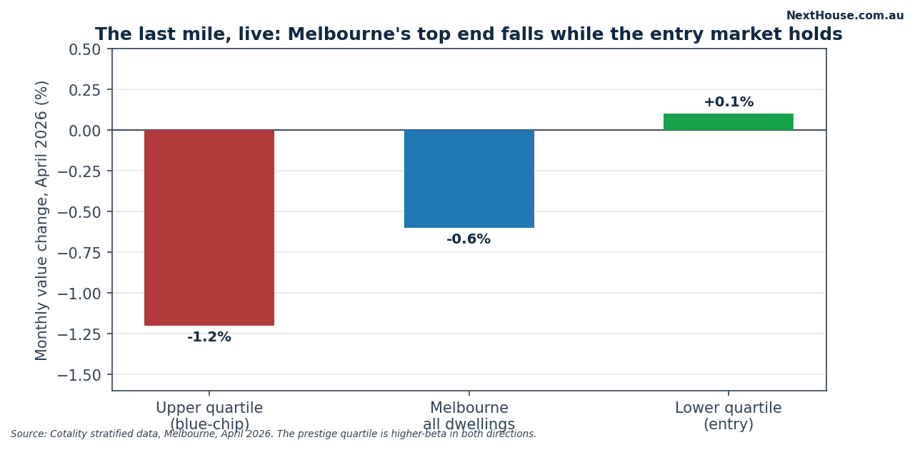

You can watch this playing out in Melbourne right now. In April 2026, the prestige upper quartile fell about 1.2% in a single month. The affordable lower quartile? Up 0.1%.

Same city. Same rate environment. Completely different outcomes.

WHAT MAKES YOUR SUBURB HIGH OR LOW BETA?

| Characteristic | More exposed (higher beta) | More sheltered (lower beta) |

| Price tier | Prestige / blue-chip | Affordable / entry-level |

| Investor share | High (CBD & student-belt units) | Low (owner-occupier suburbs) |

| Household leverage | Highly geared mortgage belts | Lower-debt, established owners |

| Land supply | Constrained, established | Supply-elastic outer corridors |

| New-supply pipeline | Apartment oversupply caps growth | Tight pipeline supports values |

| Industry exposure | Globally-geared sectors | Diversified services |

Source: NextHouse framework, built on RBA RDP 2020-02 and Cotality data.

And here’s how Melbourne’s suburbs actually map to this:

| Melbourne area | Type | Typical beta |

| Toorak, Brighton, Kew | Prestige established | High (~1.3–1.5×) |

| Carlton, Clayton, Box Hill | Investor / student apartments | High and volatile |

| Inner-east & bayside middle ring | Established owner-occupier | Around 1× |

| Melton, Wyndham, Casey | Affordable outer growth | Low (~0.4–0.6×) |

Source: NextHouse heuristic, RBA RDP 2020-02, Cotality stratified data. Beta multipliers illustrative.

The last-mile rule is simple: take the expected Melbourne-wide move, then scale it by your suburb’s beta.

WORKED EXAMPLE: THE 2025–26 MIDDLE EAST CONFLICT

Let’s run a real event through the chain.

Step 1 — Which channel? Primarily commodity (oil and energy prices up) and confidence (risk-off mood).

Step 2 — Does it reach the valve? Yes. Higher energy prices fed Australian inflation, which pushed the RBA to lift the cash rate to 4.35% in 2026. The gold path activated.

Step 3 — Will the move stick? Partly. The RBA expects fuel-driven inflation to stay elevated for about a year. This is more than a few-week scare.

Step 4 — The last mile. A higher-for-longer rate setting hits the high-beta end hardest — which is exactly why Melbourne’s prestige quartile is falling while the affordable outer ring holds.

| Step | The question to ask | What to watch |

| 1. Channel | Which of the six channels does it travel down? | Map the news to a channel |

| 2. Valve | Will it move the RBA cash rate? | The inflation print; RBA commentary |

| 3. Durability | Will the rate move stick, or unwind? | Permanent vs temporary; RBA guidance |

| 4. Last mile | What is my suburb’s beta? | Price tier, investors, leverage, supply |

Source: NextHouse decision filter.

Notice what the framework filters out. The conflict’s direct effects — shipping disruption, geopolitics, the human tragedy — are enormous as news but reach your suburb only after being converted into an interest-rate setting. The confidence shock alone, had it not moved inflation, would have faded in weeks.

The chain tells you where to look: not at the war, but at the inflation print and the RBA’s next move.

THE BULL CASE: 5 REASONS TO TRUST THIS FRAMEWORK

- The valve is measured, not guessed The cash-rate-to-price link is quantified in the RBA’s own model — about one-third for a permanent 1-point move. Few relationships in property are this well-evidenced.

- The transmission is fast here With most mortgages variable or short-fixed, rate changes reach household budgets quickly. The dominant channel is also the most responsive.

- The history fits Across 26 years, the events that moved Melbourne moved the cash rate — and the events that didn’t, didn’t. This framework is a description of what actually happened, not a theory imposed on top of it.

- The weak channels really are weak Foreign buying is tiny and now restricted. Confidence shocks fade. Commodity income reaches Melbourne only indirectly. The rankings match the data.

- The last mile is measured too The roughly four-fold spread in suburb sensitivity comes from RBA research, not intuition — so the personal step is as grounded as the macro one.

THE BEAR CASE: 5 TIMES THE CHAIN CAN SURPRISE YOU

- Domestic policy can bypass the global chain entirely The deepest Melbourne fall this century (2017–19) had no global trigger — it was APRA tightening credit. Policy can move prices with the cash rate completely unchanged.

- The valve can stick or surprise The chain is reliable in direction, not in precise timing or size. Rate moves can be faster, slower, bigger or smaller than expected.

- State and local factors increasingly dominate Melbourne’s recent underperformance is largely a Victorian story — state taxes, supply, migration. Local policy can override the national signal.

- Permanent vs temporary is hard to judge in real time The model’s big effects need rate changes to stick. Knowing whether they will — when you’re in the middle of a crisis — is genuinely difficult.

- A jobs shock would bypass the valve Mass unemployment would hit prices directly through forced sales, without waiting for the rate channel. Deep enough recession = a different kind of shock entirely.

THREE QUICK PLAYBOOKS: WORLD CRISIS

For owner-occupiers Run the filter, not the fear. If the event won’t move the cash rate, it will mostly pass through. Your suburb’s beta only matters if you’re forced to sell. The real task is protecting your buffer against rates staying higher for longer.

For investors The framework is a positioning tool. High-beta suburbs — prestige, investor-heavy, land-locked — amplify both the fall and the recovery. That suits a buyer who can time the rate cycle and hold through the rough patch. It punishes the thinly-buffered. Knowing your suburb’s beta is the difference between riding the cycle and being ridden by it.

For first home buyers The counter-intuitive truth: the best entry windows have historically opened during global gloom that triggered rate cuts — not during calm. And affordable, lower-beta suburbs move less in both directions, which makes them a steadier first step. Watch the inflation print and the RBA. Not the crisis headline.

Watch: Melbourne First Home Buyers Just Borrowed $560K — Most Will Regret It

THE KEY NUMBERS AT A GLANCE

| Figure | Why it matters |

| RBA cash rate (May 2026): 4.35% | The valve — where it sits right now |

| Permanent 100bp effect: ~−33% real prices | The valve’s full power |

| Suburb beta spread: −0.9% to −3.5% | The last mile — a ~4× range |

| Variable/short-fixed mortgages: 80%+ | Why the channel transmits fast |

| Household debt-to-income: ~177% | Why rate moves bite hard |

| Foreign buys vs turnover: $4.9B vs ~$674B | Why the capital channel is nearly irrelevant |

| Net overseas migration (2024–25): 306,000 | The slow structural demand floor |

Source: RBA, ABS, FIRB/Treasury, PEXA, Cotality.

THE NEXTHOUSE VIEW

The most useful habit you can build right now? Stop asking “how bad is this crisis?” and start asking three sharper questions:

- Which channel does it travel down?

- Will it move the cash rate?

- Will the move stick?

Then scale by your suburb’s beta. That four-step filter will give you a clearer picture than most of the commentary you’ll read — in about 10 minutes per event.

None of this is a forecast. Domestic policy or a real jobs shock can always bypass the chain. But as a lens for reading a noisy world, it’s about as reliable as Australian property analysis gets.

FAQs

- How do global events affect Melbourne house prices?

Through six possible channels — but mostly through one: interest rates. A global event reaches Melbourne primarily by changing Australian inflation and therefore the RBA cash rate, which changes borrowing capacity and prices. Events that don’t move the cash rate usually do very little to Melbourne. - Do foreign buyers drive Melbourne prices?

Far less than most people think. Foreign purchases were about $4.9B in 2022-23 against roughly $674B in national turnover — less than 1%. And foreigners have been banned from buying established dwellings since April 2025, extended through to mid-2029. It can matter for a specific new apartment project. It cannot move the Melbourne market. - Why do some suburbs fall harder than others in the same downturn?

Because of their “beta” — how sensitive they are to rate changes. RBA research shows a 100-point rate rise cuts prices in the most exposed areas about four times more than the steadiest. Higher price level, more investors, higher leverage and constrained land supply all increase sensitivity. - Which Melbourne suburbs are highest-beta?

Generally prestige, established, investor-exposed markets — Toorak, Brighton, Kew and inner-city apartment precincts. Affordable outer corridors like Melton, Wyndham and Casey tend to move much less in both directions. - Is migration a fast driver of prices?

No — it’s powerful but slow. It shows up in rents and vacancy rates long before sale prices. Net migration eased from a record 538,000 in 2022-23 to 306,000 in 2024-25. It’s a structural demand floor, not a fast transmitter of shocks. - Can a global event move Melbourne without moving the cash rate?

Rarely, and usually not for long. A pure confidence shock can dent sentiment and clearance rates for a few weeks. But for most events, no rate move means no lasting price effect.

RELATED WATCHING

- Two Global Crises Just Hit Your Melbourne Mortgage — And Nobody Is Connecting the Dots

- RBA Hikes to 4.35% on 8-1 Vote — Melbourne Property Just Split in Two

- Melbourne Property Hit a 4-Year Low — Why the RBA’s May 5 Decision Changes Everything

- Will the RBA Hike on Tuesday? Here’s What 4 Major Banks Say

- Melbourne First Home Buyers Just Borrowed $560K — Most Will Regret It

- Melbourne’s Cheap Suburbs Are Eating the Blue Chips Alive

REFERENCES

- RBA. ‘A Model of the Australian Housing Market’ (Saunders & Tulip), RDP 2019-01.

- RBA. ‘The Distributional Effects of Monetary Policy’ (He & La Cava), RDP 2020-02.

- RBA. C. Kent, ‘Interest Rates and the Property Market,’ September 2022.

- RBA. Cash rate decisions and Statement on Monetary Policy, 2025-26.

- RBA / CEIC. Household debt-to-income ratio (176.95%, Dec 2025).

- ABS. ‘Overseas Migration, 2024-25,’ released December 2025.

- FIRB / Treasury. Register of Foreign Ownership of Residential Land.

- PEXA Group. Aggregate residential sales value (~$674.5B, 2022).

- Cotality (CoreLogic). Melbourne Home Value Index, April 2026.

- APRA. Macroprudential measures; serviceability buffer.

DISCLAIMER

General information only. This article is published by NextHouse as an information service under the ASIC s.911A(2)(eb) exemption. NextHouse does not hold an Australian Financial Services Licence (AFSL) or Australian Credit Licence (ACL), and nothing here is financial, credit, investment, tax or legal advice, or a recommendation to buy, sell or hold any property.

The Global Trigger Chain is an analytical framework, not a prediction. The Saunders-Tulip ~one-third figure is the modelled long-run effect of a PERMANENT 100bp change — temporary moves are much smaller and unwind. The suburb beta spread (0.9% / 2.3% / 3.5%) is a two-year-horizon estimate; real suburbs blend offsetting characteristics.

Before acting, speak to a licensed financial adviser, registered tax agent, or an MFAA- or FBAA-accredited mortgage broker about your own circumstances.

Disclosure: NextHouse does not accept paid placement from developers, agents, councils, lenders, builders or any third party.