What if losing money on a property was actually part of the plan? Sit with that for a second — because it sounds wrong until it doesn’t. And once it clicks, you’ll start to see why so many Australians have been quietly using this strategy for years while everyone else stands around at dinner parties nodding along to a term they’ve never fully understood.

Negative gearing. Two words that come up in almost every serious property conversation in this country, and yet somehow manage to leave half the room none the wiser. The people who know it nod. The people who don’t nod anyway. And the explanation never actually comes. You don’t need a financial background to get it. You don’t need multiple properties or a hefty salary or an accountant who knows your name. You just need someone to walk you through it honestly — which is exactly what this is.

What does “gearing” even mean?

Nothing complicated about it. The “negative” part just describes what’s happening with the cash flow. Your investment property earns money — rent from your tenants. It also costs you money — the loan repayments, the property manager’s cut, council rates, insurance, the occasional repair bill. When the costs are running higher than the rent coming in, you’re making a loss on the property. That’s a negatively geared property.

And that’s genuinely the whole concept. You’re spending more than you’re earning on that investment each year. The reason it matters — and the reason so many Australians do this deliberately — is what the Australian tax system lets you do with that loss. Which is where things get interesting.

Why Would Anyone Deliberately Lose Money?

This is the question that trips most people up — and it’s a fair one. On the surface, it sounds backwards. You’ve bought an asset, you’re losing money on it every year, and somehow this is considered a good strategy?

The first is the tax benefit. In Australia, the loss you make on your investment property can be offset against your other income — your salary, your business income, whatever else you earn. That reduces your taxable income, which means you pay less tax. Every year the property runs at a loss, the ATO effectively chips in and covers part of that shortfall for you through your tax return.

The second is the long game. Nobody who buys a negatively geared property expects to lose money forever. The whole point is that you’re buying in a location where you believe the property’s value will grow over time. The annual loss is the price you pay to own that asset — and when you eventually sell, the capital gain is meant to more than cover everything you put in along the way.

Think of it like paying rent on a business premises while you’re still growing. You’re spending money now because you’re confident the payoff comes later.

A Real Example — With Actual Numbers

Say you buy an investment property that brings in $20,000 a year in rent. That’s $1,667 a month — pretty standard for a lot of regional or suburban properties around Australia.

Your costs for the year look like this:

- Loan interest: $24,000

- Property management fees: $2,000

- Council rates: $1,500

- Landlord insurance: $1,500

- Repairs and maintenance: $3,000

- Total expenses: $32,000

Roughly $500–$650 a month to hold a property that you own and that (all going to plan) is growing in value. Whether that’s worth it depends entirely on the property, the location, and how long you’re willing to hold it. But the mechanics are that simple.

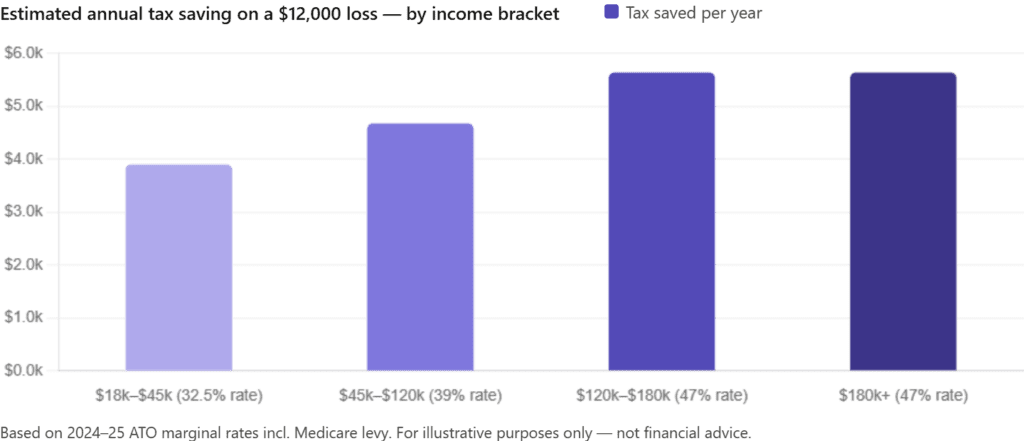

The Tax Saving Isn’t the Same for Everyone

Here’s the part most articles skip past — and it’s genuinely important. Estimated annual tax saving on a $12,000 negative gearing loss:

Based on 2024–25 ATO marginal tax rates. For illustrative purposes only — not tax advice.

Someone earning $200,000 a year saves roughly $1,700 more per year in tax than someone earning $50,000 — on the exact same property and the exact same loss.

This is why negative gearing tends to get discussed more in the context of higher earners. It’s not that it doesn’t work at lower income levels — it still does. It’s just that the tax benefit is proportionally larger the higher you climb. A person on the top marginal rate is getting 47 cents back for every dollar of loss.

Negative Gearing vs. Positive Gearing — Side by Side

Positive gearing is the other side of the coin. It’s when your rental income is higher than your costs — the property is making you money right now. That sounds better at first glance, but there’s a catch: that income gets taxed.

| Negative gearing | Positive gearing | |

| Cash flow right now | Costs you money each year | Puts money in your pocket |

| Tax impact | Reduces your taxable income | Adds to your taxable income |

| Best suited for | Long-term growth investors | Investors who need income now |

| Main risk | Relies on capital growth | Less growth-reliant, but lower returns |

| Higher income earners | Tax benefit is more valuable | Less relevant |

| When it works best | 7–10+ year hold, growth location | High-yield, stable rental markets |

Neither approach is universally better. Some investors deliberately build a mix — a negatively geared property in a high-growth corridor balanced by a positively geared property generating regular income. The strategy depends on where you are financially right now and where you want to be.

What Can You Actually Claim?

One of the most common mistakes new investors make is not realising just how many of their costs are tax-deductible. A lot of people only think about loan interest and miss everything else sitting underneath it.

Here’s the full list of common claimable expenses:

- Interest on your investment loan — this is usually the biggest one by far, and it’s fully deductible.

- Property management fees — if you use a property manager (which most investors do), their fees are claimable.

- Repairs and maintenance — fixing a broken hot water system, patching a leaky roof, repainting between tenants. These are deductible in the year you pay them.

- Council rates and water rates — fully deductible.

- Landlord insurance — deductible.

- Depreciation — this one trips people up because it’s not a cash expense. You don’t physically pay depreciation — it’s the estimated wear and tear on the building and its fixtures over time. But you can claim it on your tax return, and it can add thousands of dollars to your deduction. A quantity surveyor’s depreciation schedule is worth every cent.

- Accounting fees — the fees you pay your accountant specifically for managing the investment property are deductible too.

Add all of these up, and the gap between your rental income and your total costs is usually larger than people expect — which is exactly what tips a property into negative gearing territory.

The Risks — And There Are Real Ones

Negative gearing has genuine merit as a long-term strategy. It also has real risks, and anyone who tells you otherwise is selling something.

Fund the Gap – The tax saving comes at the end of the financial year. The shortfall has to be funded month by month, right now. If your income drops — redundancy, reduced hours, health issues — you’re still on the hook for that gap. Before you commit to any negatively geared property, you need to be honest about whether you can sustain this payment in a bad year, not just a good one.

Capital Growth – If the property doesn’t grow in value, or grows very slowly, you’ve spent years funding a shortfall and the numbers don’t add up. Negative gearing is not a strategy that works on any property anywhere — it only works on properties in locations with genuine long-term growth potential. Location selection isn’t just important, it’s everything.

Interest Rates — more seriously than most first-time investors do. When rates go up, your loan repayments go up with them, which means the gap between what the property earns and what it costs you gets wider. A property that sits comfortably within your budget at 5% can start to feel like a different commitment entirely at 6.5% or 7%. Before you buy, run the numbers at a rate higher than whatever the bank is quoting you today. Not because rates will definitely rise, but because they might — and you want to know the answer before it becomes a problem, not after.

Policy Risk – Negative gearing has come up in Australian political debate more times than most investors would like — there have been genuine proposals to wind it back or restrict it, and those conversations tend to resurface every election cycle. Nothing has changed yet, and it remains a fully legal and widely used strategy. But tax policy does shift over time, and any strategy built heavily around a single tax benefit carries some exposure to that.

Is Negative Gearing the Right Move for You?

Genuinely depends. Not a cop-out answer — it actually does.

The strategy tends to suit investors who have stable, consistent income they can rely on to cover the annual shortfall without financial stress. And it suits people who have sat down with a proper accountant and stress-tested the numbers against their real financial situation — not just a back-of-the-napkin estimate.

It’s less suitable for investors who are already stretched thin and can’t comfortably absorb the monthly gap. It’s less suitable for people who need cash flow from their investments right now — if you need the money to live on, a positively geared property or a different asset class is a more sensible starting point. And it’s less suitable for properties in flat or declining markets, where the growth premise that underpins the whole strategy simply doesn’t exist.

A Quick Summary Table

| Question | The short answer |

| What is negative gearing? | When your property costs more than it earns — and you use the loss as a tax deduction |

| Why do it? | Tax deductions reduce your bill now; capital growth builds wealth later |

| Who benefits most from the tax side? | Higher-income earners — their marginal rate makes each deduction worth more |

| What can you claim? | Loan interest, management fees, council rates, insurance, repairs, depreciation, accounting fees |

| Biggest risk? | Funding the annual shortfall if income drops, and relying on growth that doesn’t come |

| Minimum hold horizon? | 7–10 years, realistically |

| Is it right for everyone? | No — get professional advice for your specific situation |

Final Thought

Negative gearing is not a trick. It is not a loophole. It is a legal, widely used, government-sanctioned investment strategy that sits inside the Australian tax system by design — and millions of Australians have used it to build serious long-term wealth. But it works best when you go in clear-eyed. You need the right property in the right location. You need the financial runway to fund the shortfall through the lean years. You need a long enough time horizon for the capital growth to do what it’s supposed to do. And you need a qualified accountant who actually looks at your numbers — not someone else’s hypothetical scenario, but yours.

Done right, with all of those things in place, a negatively geared property can be one of the more powerful tools in a long-term investment strategy. Done carelessly, it’s an expensive lesson.

Thinking about getting into investment property — or building on what you already have? Get in touch with NextHouse. We would help you understand your options and a strategy that could actually fit your goals.

Disclaimer: This article is here to inform and educate, not to tell you what to do with your money. Everyone’s financial situation is different, and nothing here should be taken as financial, investment, or legal advice. Before making any property decisions, it’s always worth sitting down with a qualified professional who knows your full picture.