If you’re renting in Melbourne and quietly doing the math every time your lease comes up for renewal, this is the article you’ve been waiting for. Because here’s the thing nobody’s telling you straight: yes, there really are suburbs where your mortgage would be cheaper than your rent — but it’s not the outer-suburb house you’ve been eyeing on realestate.com.au. It’s almost always a unit, and it’s almost always closer to the city than you’d guess.

And even when the numbers line up perfectly in your favour, there’s still one wall standing between you and that cheaper life: the deposit. Renters are now handing over a record share of their income just to keep a roof over their heads, which makes saving that lump sum harder every single year — even when buying would leave them better off month to month.

Quick answer (TL;DR)

- It’s almost always units, not houses. Only 1 in 60 house markets beat renting. Almost 1 in 5 unit markets do.

- The suburbs on this list are inner-city units like Carlton, the CBD, Flemington and Southbank — not Melton, Tarneit or Cranbourne.

- Even on these “cheaper to buy” units, you still need a deposit. And that’s the actual trap. Renters are paying a record share of their income in rent, which makes saving that deposit harder every year.

- A 5% deposit scheme can fix this almost overnight, if you qualify.

Read on for the suburb list, the real costs, and what to actually do about it.

The one rule that decides everything

Forget the suburb names for a second. There’s one simple test that tells you whether buying beats renting on a month-to-month basis:

Is the suburb’s rental yield higher than your mortgage rate?

If a property’s yield is above the mortgage rate, the rent it could earn covers more than the interest on the loan — so owning works out cheaper. If the yield sits below the mortgage rate, renting stays the cheaper option, no matter how painful the rent feels.

With mortgage rates sitting around 5.9% in mid-2026, that number is the line every suburb gets measured against.

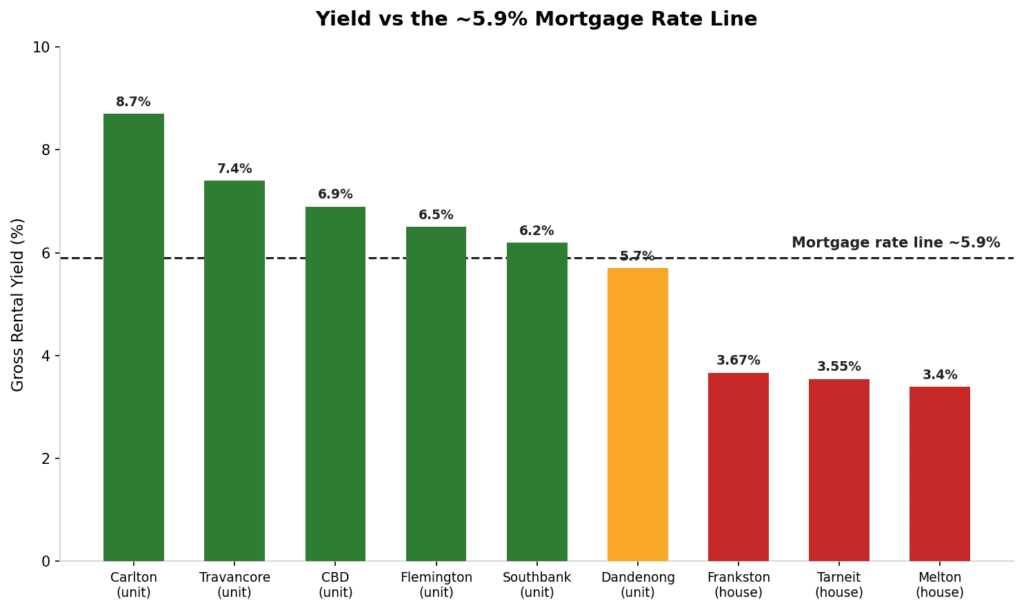

Figure 1: Green suburbs clear the 5.9% mortgage rate line (cheaper to buy). Red suburbs sit below it (cheaper to rent).

| What you’re looking at | Example | What it means |

| Yield ABOVE mortgage rate | Carlton unit ~8.7% vs ~5.9% | Buying is cheaper than renting |

| Yield BELOW mortgage rate | Melton house ~3.4% vs ~5.9% | Renting stays cheaper |

| The line itself | ~5.9% owner-occupier rate, mid-2026 | The number every suburb is tested against |

Why this is a unit story, not a house story?

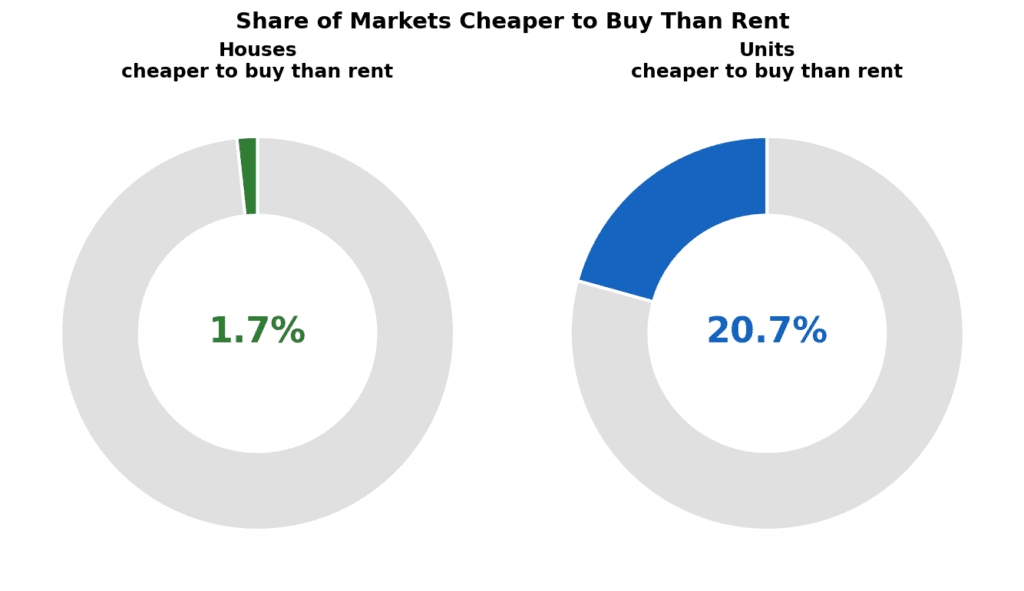

Here’s the part most people get wrong. They picture an outer-suburb house when they hear “renting costs more than buying.” It’s actually the opposite. Across the capital cities, only 1.7% of house markets are cheaper to buy than rent. For units, that number jumps to 20.7% — roughly one in five.

Figure 2: Units are roughly 12 times more likely than houses to be cheaper to buy than rent.

Why? Simple supply and demand. So unit rents kept climbing while unit prices stayed flat. Low prices plus high rents equals high yields — and high yields are exactly what tips the scale toward buying.

In fact, in March 2026, Melbourne’s median unit rent ($600 a week) overtook the median house rent for the first time ever.

The 20 suburbs where renting now costs more

Here’s the working list — roughly 20 Melbourne markets where the typical mortgage repayment (on a 20% deposit) sits at or below the typical rent. Treat this as a shortlist to check yourself, not a buy signal.

| Tier | Suburbs (mostly units) | Why they’re on the list |

| Strong case | Carlton, Travancore, CBD/Melbourne City, Flemington, Southbank, West Melbourne, North Melbourne, South Melbourne, Richmond, Abbotsford, Essendon, Notting Hill | Yields of 6–9% comfortably clear the mortgage rate |

| Borderline | Bundoora, Epping, Sydenham, Mill Park, Broadmeadows, St Albans, Dandenong, Craigieburn | Yields of 4.5–5.7% — close to the line, full costs decide it |

| Doesn’t make the cut | Melton, Tarneit, Werribee, Cranbourne, Frankston (houses) | Yields of 3.4–4% — renting stays cheaper |

Carlton is the standout example: a typical unit there costs around $1,749 a month to own versus $2,386 a month to rent. That’s not a typo — owning really is over $600 a month cheaper there right now.

Why outer suburb houses miss the list?

This is worth slowing down on, because it surprises a lot of people. Take a $500,000 house in Melton, renting for about $420 a week ($1,820 a month). That feels expensive as a renter. But the mortgage on that same house, with a 20% deposit at 5.95%, runs about $2,385 a month — already higher than the rent, before you’ve added a single other cost.

Outer suburb yields tell the same story everywhere: Werribee around 3.65%, Tarneit 3.55%, Frankston 3.67%, Melton about 3.4%. All sit well under the 5.9% mortgage rate line. These suburbs are bought for long-term growth, not for saving money on rent right now — and that’s a fair reason to buy, but it’s a different reason than the one this article is about.

What owning really costs (beyond the mortgage)?

Every “cheaper to own” number above only counts the mortgage. A fair comparison needs to add the costs renters never pay: council rates, insurance, maintenance, and — for units — owners corporation fees.

| Extra ownership cost | House (per year) | Unit (per year) |

| Council rates | $1,800 – $4,000 | $1,200 – $2,200 |

| Building/contents insurance | $1,800 – $2,600 | Usually bundled in OC fee |

| Maintenance (roughly 1% of value) | $5,000 – $9,000 | Partly covered by OC fee |

| Owners corporation fees | Not applicable | $1,000 – $5,000+ |

| Stamp duty (upfront, non-first-home-buyer) | $25,000 – $44,000 | $25,000 – $44,000 |

Add these costs to the Melton example, and owning jumps to roughly $3,200 a month against $1,820 in rent — renting wins easily there. But run the same test on a high-yield Carlton unit, and owning still comes out ahead, because the yield is so far above the mortgage rate that even these extra costs can’t close the gap.

The single biggest cost to check before you trust any “cheaper to own” number is the owners corporation fee. On a luxury tower with a pool and gym, this can run past $8,000 a year — enough to flip the whole comparison back in favour of renting.

The real trap: it’s the deposit, not the repayment

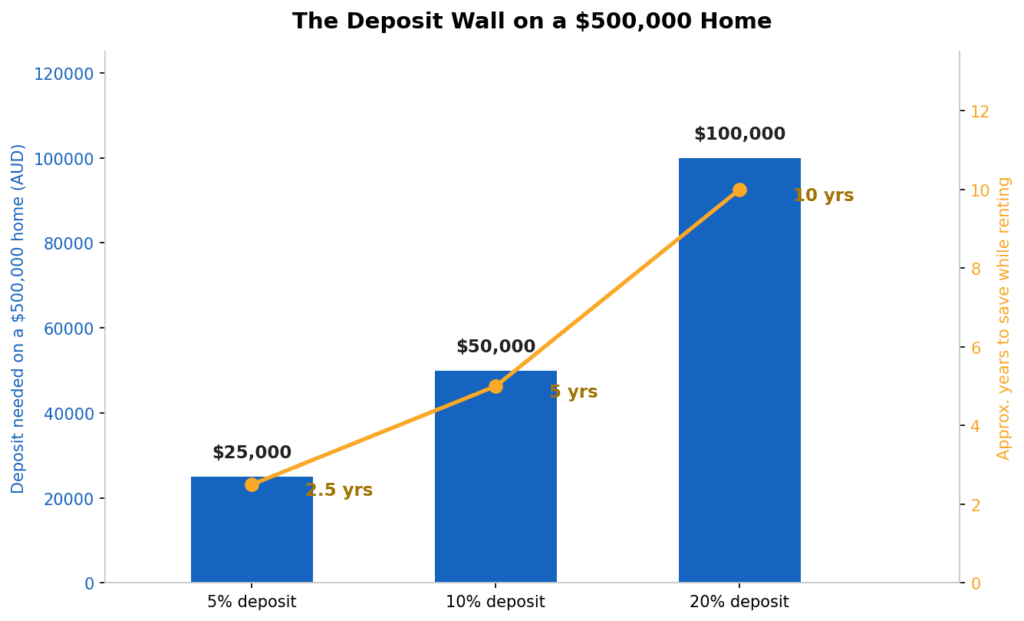

Here’s the part that actually matters most. Say you’ve found one of the genuine suburbs — a Carlton unit that’s cheaper to own even after all the extra costs. To get there, you still need a deposit and stamp duty upfront. And that’s where most renters get stuck.

Figure 3: The deposit, not the monthly repayment, is what actually keeps most renters out.

Why renters can’t save fast enough?

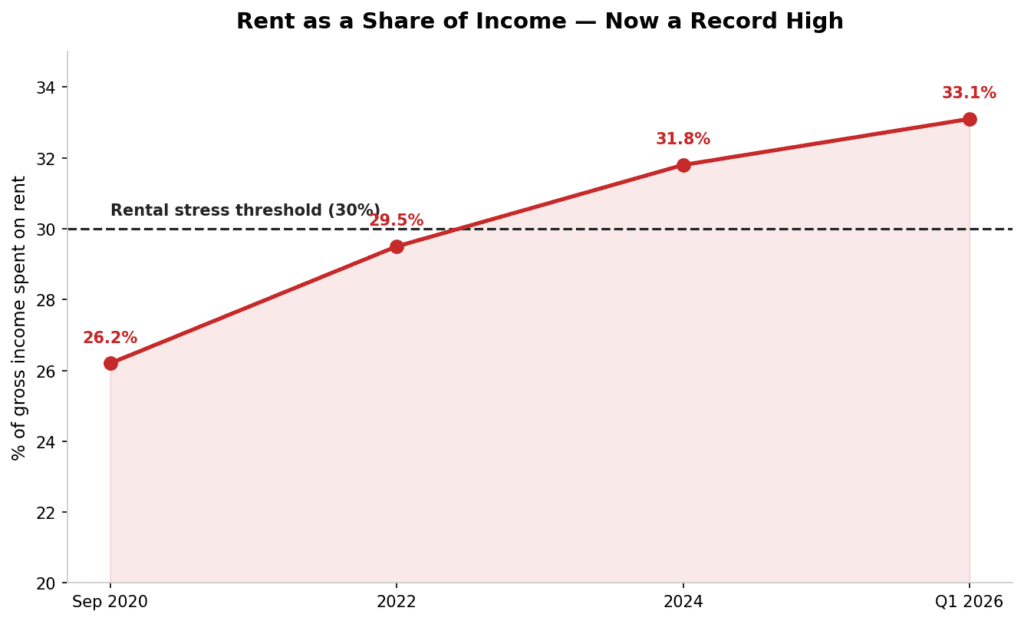

This trap isn’t bad luck. It’s mechanical. Anything past 30% of income on rent is considered rental stress — and the average renter is now well past that line. This is the trap, in one line: high rent stops you saving the deposit that would let you escape the high rent.

Figure 4: With vacancy around 1.6%, renters have almost no room to negotiate, so this share keeps climbing.

This is the trap, in one line: high rent stops you saving the deposit that would let you escape the high rent.

The schemes that can get you there sooner

If the deposit is the wall, government schemes are the ladder. And in 2026, that ladder got a lot taller.

| Scheme | What it does | Why it matters |

| First Home Guarantee | 5% deposit, no LMI, no income cap, $950k Melbourne price cap | Cuts the deposit wall from 20% down to 5% |

| Victorian stamp duty exemption | $0 duty up to $600k, concession up to $750k | Removes tens of thousands in upfront cost |

| First Home Owner Grant | $10,000 for new homes up to $750k | Extra cash toward the deposit |

| Help to Buy (shared equity) | 2% deposit, government takes 30–40% equity | The lowest deposit route, smaller loan |

| Off-the-plan duty concession | Lowers dutiable value on apartments | Helps units stay under the $600k/$750k threshold |

Put these together, and a first home buyer could pick up a $590,000 unit in a genuinely cheaper-to-own suburb with about $29,500 upfront — no LMI, no stamp duty. That’s the deposit wall actually coming down. The trade-off: a smaller deposit means a bigger loan, so you’re more exposed if interest rates move.

Should you switch? The case for and against

Reasons it might make sense:

- In the right unit suburbs, owning genuinely costs less than renting, even after every extra fee

- Rent builds zero equity for you — the same money on your own loan builds equity from day one

- The 5% deposit scheme removes most of the upfront barrier

- Unit supply has kept entry prices low, with fewer new apartments being approved going forward

- You get certainty of tenure — no more lease renewals or rent hikes

Reasons to stay cautious:

- This price gap may not last. If rates rise as forecast, the advantage shrinks

- A high owners corporation fee can wipe out the entire saving

- Units have historically grown slower than houses, and some buildings face costly special levies (cladding repairs have cost some owners $20,000–$50,000)

- A 5% deposit means a bigger loan and more exposure if rates move — always stress-test repayments at 6.5–7%

- Change the deposit, rate or loan term, and the whole comparison can flip

What to do next, based on who you are?

If you’re renting and thinking about buying: Start with the one rule — is the yield in the suburb you’re considering above today’s mortgage rate? That only really happens in high-yield unit markets, so look there first, not at outer houses. Then check the full costs, including owners corporation fees, before you get excited.

If you’re a first home buyer: The 5% deposit scheme plus the Victorian stamp duty exemption could get you into a sub-$600k unit with around $30,000 upfront. Ask for the Section 32 and the owners corporation certificate before you commit, and stress-test your repayments at a higher rate than today’s.

If you’re an investor: The same high-yield unit suburbs that beat renting for owner-occupiers also tend to give investors the strongest cash flow. The trade-off is slower capital growth and special-levy risk — read the building’s financial records, not just the suburb’s yield.

Watch next on YouTube: Melbourne Rental Crisis 2026: Why 21,000 Properties Vanished in One Year

The NextHouse View

The “renting now costs more than owning everywhere” headline isn’t true, but the real version is far more useful. This gap is real, and it’s narrow, and it lives almost entirely in high-yield inner Melbourne units — not the outer houses most people assume. The one number that decides it is the yield against your mortgage rate, and the one cost most people forget is the owners corporation fee, which can erase the whole advantage on its own.

But here’s the part I think gets missed every time this story comes up: the real barrier was never the monthly payment. It’s the deposit and the stamp duty that record-high rents stop people from ever saving. That’s exactly why the 5% deposit scheme matters more than any suburb on this list — it’s the thing that actually breaks the trap open.

FAQs

- Why are units cheaper to buy relative to rent than houses?

A decade of apartment building kept unit prices low, while a tight rental market pushed unit rents to record highs. That combination creates high yields, which is what tips the scale toward buying. - Is it cheaper to rent or buy in Melbourne in 2026?

In high-yield inner unit markets — Carlton, Travancore, the CBD, Flemington, Southbank — owning is now cheaper than renting, even after every extra cost. - Does “cheaper to own” include every cost?

Often not. Most headline numbers only count the mortgage on a 20% deposit. A fair comparison adds rates, insurance, maintenance and owners corporation fees — which can erase the advantage outside the highest-yield suburbs. - What’s the real “rental trap”?

The deposit, not the weekly repayment. Even where owning is cheaper month to month, you still need a lump sum to get there — and renters are now spending a record 33% of income on rent, which makes saving that lump sum extremely hard. - How does the First Home Guarantee help?

It lets eligible first home buyers purchase with just a 5% deposit and no Lenders Mortgage Insurance, with no income cap and a $950,000 Melbourne price cap. It turns a 20% deposit wall into a 5% one. - Should I buy a unit just because it’s cheaper than renting?

Not on cost alone. Units tend to grow more slowly than houses and can face large one-off levies (cladding repairs have cost some owners $20,000–$50,000). Always check the building’s financials and the Section 32 first.

References

- Cotality (CoreLogic). Buy-versus-rent analysis, March 2026.

- Cotality (CoreLogic). Home Value Index, Melbourne, May 2026.

- Cotality (CoreLogic). Rental Review, Q1 2026.

- Domain. Rent Report, March quarter 2026.

- Domain. Suburb-level buy-vs-rent analysis.

- SQM Research. Melbourne rents and vacancy rate, May 2026.

- Real Estate Institute of Victoria. Median prices, March 2026 quarter.

- Reserve Bank of Australia. Cash rate target, June 2026.

- Westpac and major bank mortgage rate schedules, 2026.

- State Revenue Office Victoria. Land transfer duty rates and exemptions.

- Housing Australia. First Home Guarantee, expanded scheme from October 2025.

- Australian Government / vic.gov.au. Help to Buy shared equity scheme.

- Department of Treasury and Finance Victoria. Victorian Homebuyer Fund.

- Victorian Government. First Home Owner Grant and off-the-plan duty concession.

- CoreLogic. Carlton unit worked repayment-vs-rent example, March 2025.

- ANZ-CoreLogic. Housing Affordability Report.

- Cotality commentary on five-year rent growth and the buy-vs-rent gap.

- Victorian owners corporation fee data, 2025–26.

- Victorian cladding remediation cost estimates.

- ABS. Residential Property Price Indexes, 2026.

Related reading

- NextHouse — The Global Trigger Chain: how world events flow to your Melbourne suburb

- NextHouse — The “missing middle”: why Melbourne under-supplies the homes people actually need

- NextHouse — First Home Guarantee 2026: the 5% deposit scheme explained

- NextHouse — Reading owners corporation fees: the hidden cost that breaks a deal

- NextHouse — Stamp duty in Victoria: what first home buyers really pay

- NextHouse Free Reports — Get the monthly property data brief by email

Disclaimer

This article is general information only, published by NextHouse under the ASIC s.911A(2)(eb) exemption. We don’t hold an AFSL or ACL, so nothing here is financial, credit, or tax advice — and it’s not a tip to buy, sell, rent, or use any government scheme. Always check with a licensed adviser, tax agent, or accredited mortgage broker before you act, and confirm scheme rules directly with the relevant government body.

The numbers above assume a 20% deposit, a mortgage rate around 5.75–5.95%, and a 30-year loan. Change any of those and the answer can change too. Prices, yields, and rates move — so treat these figures as a guide, not gospel, and check current numbers before you decide anything. For units specifically, always get the Section 32 and owners corporation certificate, since fees and building risks vary a lot from one block to the next.