Everyone’s talking about that 93% number of Aussie investors. PropTrack dropped a report in March saying 93% of Australian investor resales in late 2025 turned a profit. Highest level in over a decade. Sounds amazing, right? Here’s the problem. That number is real — but it’s also misleading if you’re a flipper. It doesn’t count tax. It doesn’t count renovation costs. It doesn’t count what the ATO actually does to repeat flippers behind the scenes.

And with the RBA just hiking rates to 4.35% on 5 May 2026, the math for flippers has gotten harder — fast. So let’s actually work through it. No jargon. No spin. Just the real numbers.

The Four Numbers That Tell the Whole Story

Before anything else, you need four numbers in your head.

- 93% — the share of Australian investor resales in late 2025 that made a gross profit (PropTrack-Westpac Investor Report 2026). Real number. Gross number. Doesn’t survive tax.

- 6.26% — the average new variable investor rate today, after the RBA’s cumulative 75 basis points of hikes in 2026 (Feb + Mar + May). Up from 5.51% before February.

- -0.6% — Melbourne dwelling values over the March 2026 quarter. Melbourne is back in decline. Median dwelling now sitting at $828,249, which is 1.3% below the March 2022 peak.

- 47% — the marginal tax rate most repeat flippers pay on every dollar of profit. Not 23.5% with the CGT discount. 47%. Full ordinary income. Because the ATO classifies them as traders, not investors.

These four numbers sit in direct tension with each other. Understanding how they interact is what separates investors who actually make money from the ones who think they did.

Watch: Will the RBA Hike on Tuesday? Here’s What 4 Major Banks Say

Why Holding Costs Hurt More Than You Think

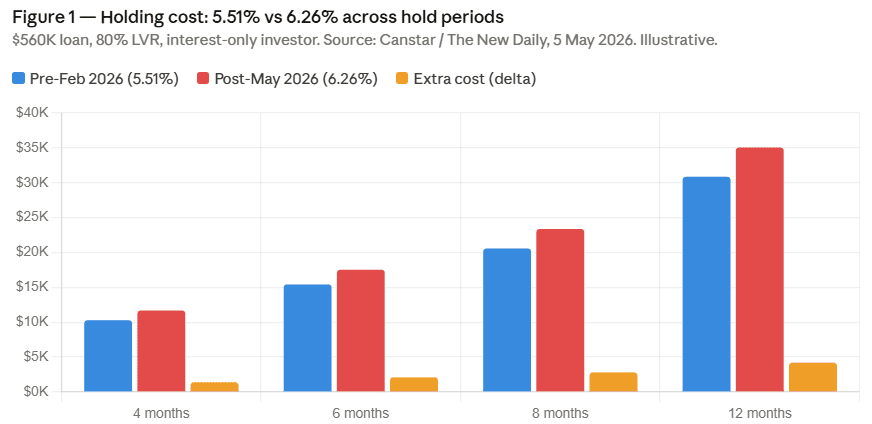

Let’s run the actual numbers on a Melbourne flip. You buy a $700,000 property at 80% LVR — so you’ve got a $560,000 loan. You plan to flip it in 8 months.

Before the February 2026 hike, your investor variable rate was around 5.51%. That 8-month flip cost you $20,571 in interest. After the May 2026 hike, your rate is 6.26%. Same flip now costs you $23,371 in interest. That’s $2,800 more — just from this year’s rate hikes alone.

Holding Cost Comparison: Pre-Feb 2026 vs Post-May 2026

| Hold Period | Cost @ 5.51% | Cost @ 6.26% | Extra Cost |

| 4 months | $10,285 | $11,686 | +$1,400 |

| 6 months | $15,428 | $17,528 | +$2,100 |

| 8 months | $20,571 | $23,371 | +$2,800 |

| 12 months | $30,856 | $35,056 | +$4,200 |

$560K loan, 80% LVR, interest-only investor. Source: Canstar / The New Daily, 5 May 2026. Illustrative model.

The APRA Wall Most Flippers Are Hitting Right Now

On 1 February 2026, APRA switched on its debt-to-income lending cap. Banks can now only write 20% of new mortgages at a DTI of 6x or above.

Here’s why this hits flippers harder than regular investors. Say you’ve got a $200,000 household income and a $1.2 million home loan on your own house. You want to borrow another $560,000 for a flip. Your combined DTI is 6.8 times — straight into the restricted bucket that banks ration tightly every quarter.

A buy-and-hold investor in the same income bracket, buying their first investment property at $700K? DTI of 2.8 times. Plenty of room. The result is that flippers who need fast approvals are getting pushed toward non-bank lenders — Pepper, Liberty, Resimac. And those lenders charge 1% to 2.5% above the major bank rate. So instead of borrowing at 6.26%, you’re borrowing at 7.5% to 9%. That compounds the rate hike problem significantly.

Watch: 214,700 Aussie Investors Just Hit APRA’s New 6× Wall

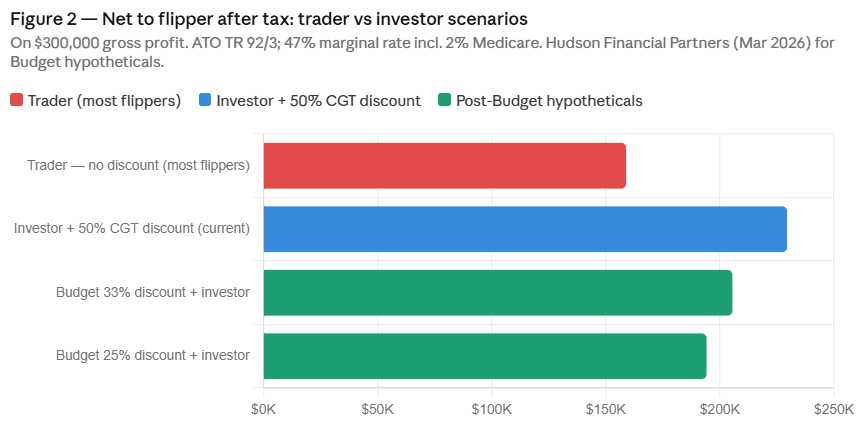

That 93% Number Doesn’t Survive Tax

Here’s where most flipping commentary gets it completely wrong. The PropTrack 93% figure measures gross profit — sale price versus purchase price. It does not subtract renovation costs, agent fees, holding costs, stamp duty, or tax. For a buy-and-hold investor selling after 12+ months, the 50% CGT discount applies.

For a repeat flipper? The ATO classifies them as a trader under Taxation Ruling TR 92/3. No CGT discount. No main residence exemption. That gap alone wipes out the margin on a lot of marginal flips.

Net-of-Tax Outcomes on $300,000 Gross Profit

| Scenario | Taxable Amount | Tax | Net to Flipper |

| Trader — full marginal rate (most flippers) | $300,000 | $141,000 | $159,000 |

| Investor + 50% CGT discount (current law, 12+ months) | $150,000 | $70,500 | $229,500 |

| Post-Budget hypothetical 33% discount + investor | $201,000 | $94,470 | $205,530 |

| Post-Budget hypothetical 25% discount + investor | $225,000 | $105,750 | $194,250 |

Illustrative model. ATO TR 92/3 + 47% marginal rate incl. 2% Medicare. Hudson Financial Partners (28 March 2026) for Budget hypotheticals.

Two things land hard here.

- First — even the worst-case Budget CGT cut still leaves a buy-and-hold investor better off than a trader-classified flipper. By a lot.

- Second — the May 12 Budget CGT review that everyone is panicking about? It barely affects flippers. Most were never eligible for the discount in the first place.

Watch: $247 Billion. 26 Years. 6 Reform Scenarios. What the CGT Discount Change Means for Melbourne

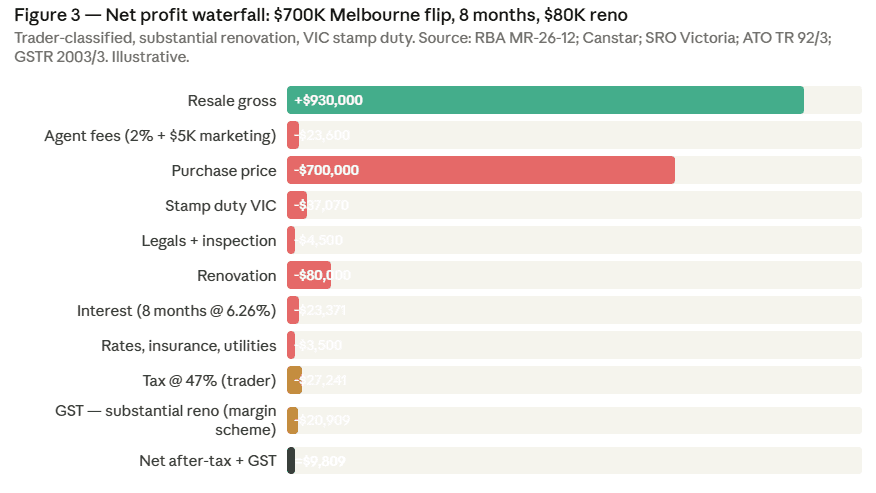

Melbourne Is Down. But Not Everywhere.

The Cotality April 2026 data shows Greater Melbourne down 0.2% in March, down 0.6% for the quarter. That’s the aggregate number. It hides a very different picture at the corridor level.

Bottom quartile dwellings in Melbourne rose 0.7% in Q1 2026. Top quartile fell 1.6%. That’s a 2.3 percentage point gap in a single quarter. At the SA3 level, it’s even clearer:

Melbourne SA3 Annual Capital Growth (Cotality April 2026)

| SA3 Corridor | Annual Growth |

| Frankston | +11.3% |

| Keilor | +9.5% |

| Sunbury | +9.0% |

| Brimbank-West | +8.6% |

| Tullamarine-Broadmeadows | +7.5% |

| Casey-South (Clyde North) | +6.7% |

| Cardinia (Pakenham) | +6.6% |

| Whittlesea-Wallan | +5.5% |

| Inner East — top quartile | -1.6% |

Source: Cotality HVI April 2026, data to 31 March 2026.

Every Melbourne SA3 with real growth is outer corridor. Every underperforming SA3 is inner east. Toorak, Hawthorn, Camberwell — structurally exposed to the APRA DTI cap and losing capital value at the same time. They’re not flip targets in 2026 at any rate.

Watch: The 10 Melbourne Suburbs Winning the RBA Hike (and 1 to Avoid)

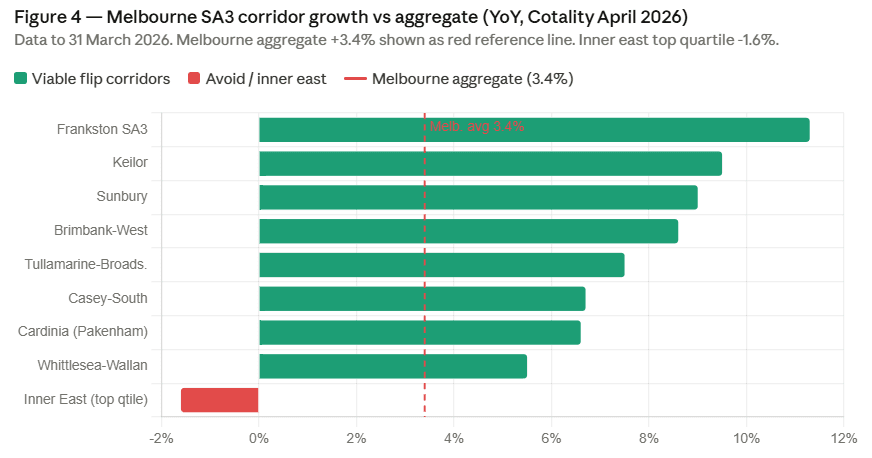

The GST Trap Nobody Talks About

Here’s the second tax layer that catches flippers off guard. If your renovation is “substantial” — meaning you’ve essentially stripped and replaced all or most of the building — the ATO treats your sale as a sale of “new residential premises” under the GST Act. That means GST on top of income tax.

The good news: the margin scheme reduces the damage. On a $700,000 purchase resold for $1.13 million, GST under the margin scheme is roughly $39,090 instead of $102,727 without it. Still a $39,000 hit. The line between cosmetic and substantial renovation matters enormously here. Paint, floors, and new taps? Cosmetic — no GST. Full strip-out, wall relocation, structural extension? Substantial — GST applies.

The renovation scope decision is a tax structuring decision, not just a budget decision. Get a quantity surveyor’s classification before you start work — not during an ATO review.

The Real Numbers: What a Melbourne Flip Actually Returns

Let’s put the whole cost stack together. This is the number most flipping commentary never shows you.

Full Net Profit Waterfall: $700K Melbourne Flip, 8 Months, $80K Reno, $930K Resale

Source: RBA MR-26-12; Canstar via The New Daily, 5 May 2026; SRO Victoria; ATO TR 92/3; GSTR 2003/3. Illustrative model.

A “good” Melbourne flip — 19% gross uplift, competently executed in 8 months — returns $9,809 net if you’re trader-classified and crossed the substantial renovation threshold. That’s not a headline you’ll see in most flipping content.

The deal only works when: (a) the renovation stays cosmetic so you dodge GST entirely, (b) you execute in under 6 months to cut holding costs, (c) the gross uplift is above 22%, or (d) you’re structured through a company at 25–30% corporate tax rate instead of 47% personal rate.

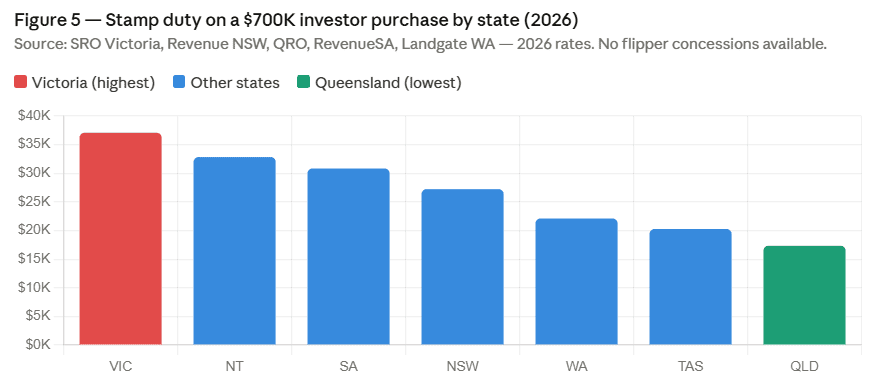

Stamp Duty: Melbourne’s Silent Deal Killer

Victoria has the highest stamp duty of any major state for a $700,000 investor purchase. Full stop.

Stamp Duty on a $700K Investor Purchase by State (2026)

| State | Stamp Duty | Effective Rate |

| Victoria | $37,070 | 5.30% |

| New South Wales | $27,220 | 3.89% |

| South Australia | $30,830 | 4.40% |

| Queensland | $17,325 | 2.48% |

| Western Australia | $22,090 | 3.16% |

Source: SRO Victoria, Revenue NSW, QRO, RevenueSA, Landgate WA — 2026 rates.

That $37,070 in VIC stamp duty means Melbourne flippers need the property to gain 5.3% in value just to break even on entry costs — before a single dollar of renovation, interest, or tax.

At Melbourne’s current aggregate growth rate of 3.4% per year, recovering stamp duty alone takes over 18 months of passive appreciation. Most flips don’t have that runway.

Where Flipping Still Works at 4.35%?

The math points to a narrow but real opportunity set. Melbourne Corridor Flip Economics (Illustrative, Cosmetic Reno Only, 6-Month Hold)

| Corridor | Median Mar-26 | YoY Growth | Typical Buy | Resale Uplift | Net Trader |

| Frankston SA3 | $720K | +11.3% | $620K | 20–25% | $35K–$55K |

| Sunbury | $680K | +9.0% | $580K | 18–22% | $30K–$45K |

| Brimbank-West | $720K | +8.6% | $620K | 18–22% | $30K–$45K |

| Pakenham (Cardinia) | $700K | +6.6% | $600K | 15–18% | $20K–$35K |

| Clyde North (Casey-S) | $760K | +6.7% | $660K | 12–16% | $15K–$30K |

Source: Cotality SA3 medians, March 2026. Net trader estimates assuming 6-month hold, cosmetic reno, 47% marginal rate, VIC stamp duty. Illustrative.

Frankston, Sunbury and Brimbank-West are the three Melbourne corridors with enough annual growth to absorb 6.26% holding costs and 47% trader tax and still leave real money in your pocket.

Pakenham and Clyde North only work if you get in below market — off-market or distressed sale. On-market at standard prices, margins get very thin very quickly. Inner east? Don’t bother in 2026.

Watch: The Metro Tunnel Just Moved Melbourne Property +9.2%. Here’s Where

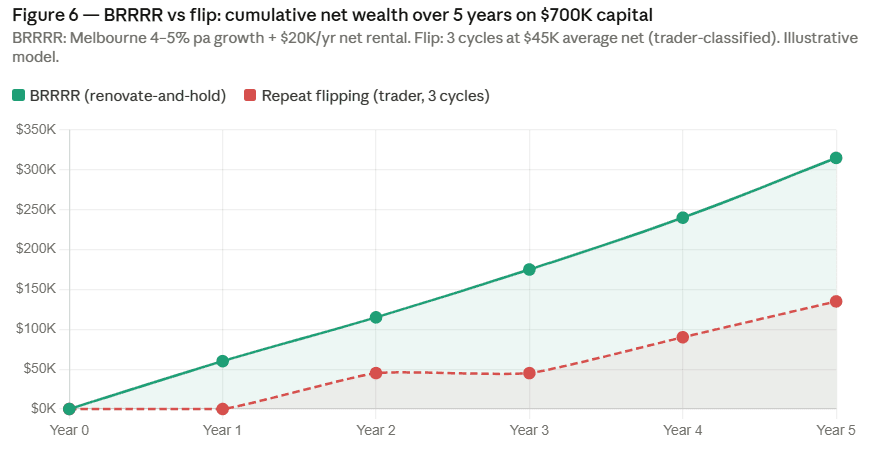

Flip or BRRRR? The 5-Year Wealth Comparison

The biggest strategic question at 4.35% isn’t whether flipping works. It’s whether flipping beats the renovate-and-hold alternative on the same capital. The BRRRR model — Buy, Renovate, Refinance, Rent, Repeat — runs the same renovation alpha as flipping, but keeps the asset. You refinance against the higher post-renovation valuation, pull your deposit back out, and let the property keep compounding.

BRRRR vs Flip: 5-Year Wealth Comparison on $700K Capital

| Strategy | 5 Year Wealth | Asset Retained? |

| BRRRR: renovate and hold | $260,000–$370,000 | Yes |

| 3 flip cycles: trader classified | ~$135,000 | No |

| BRRRR advantage | ~$185,000 | — |

Illustrative model. BRRRR assumes Melbourne 4–5% pa capital growth + $20K/yr net rental. Flip assumes $45K average net per cycle, 3 cycles over 5 years. Source: NextHouse model.

The $185,000 gap exists for two structural reasons. First, the BRRRR asset keeps compounding indefinitely. Second, the eventual BRRRR sale gets the 50% CGT discount — which trader-classified flippers can never access.\

Flipping wins only if you need end-of-cycle liquidity, if the property genuinely can’t be tenanted, or if you have specialist off-market acquisition access that others don’t. For most experienced investors with stable income? BRRRR dominates flipping at every rate environment. And the gap widens as rates rise.

Flip Strategy Scorecard at 4.35%

Not all flip strategies fail equally. Here’s how the six main approaches sit right now.

Flip Strategy Viability at 4.35% Cash Rate

| Strategy | Viability | Why |

| Cosmetic flip, sub-$700K outer corridor | Selectively viable | Avoids GST; fast hold cuts costs; ATO trader risk remains |

| Structural flip (full reno, layout change) | Marginal | Triggers GST; longer hold; construction inflation +4.2% YoY |

| Subdivision flip | Selectively viable | Higher upside but 18+ months and complex tax |

| Distressed sale / mortgagee / deceased estate | Strongest | Built-in discount removes reliance on market growth |

| BRRRR (buy-renovate-rent-refinance-repeat) | Strongest | Avoids trader classification; CGT discount preserved |

| Off-market flip via buyer’s agent | Strongest | 5–10% discount offsets entire 75bp rate hike |

The Global Picture: US and UK Are Already There

Australia isn’t operating in a vacuum. The US and UK are running the same experiment ahead of us. Average hold: 160 days. The UK Hamptons Flipping Index for 2025: the flipped share of UK home sales hit 1.5% — a decade low. Gross profit has fallen 55% over the past decade. Stamp duty now eats 43% of the average flipper’s gross return.

Australia’s 93% profitable resale rate looks good compared to both. But both markets looked good a decade ago too. The secular trend is clearly downward. If you’re planning a 5-year flipping career, expect Australian unit economics to converge toward the US and UK over time.

The Bull Case: Five Things That Still Work

- Outer-corridor growth is real — Frankston +11.3%, Sunbury +9.0%, Brimbank +8.6% against Melbourne’s aggregate 3.4%

- Sub-$650K stock has twin demand from investors AND first home buyers — compressing time on market

- Off-market acquisition discounts of 5–10% exist for disciplined operators and wipe out the entire 75bp rate hike in a single deal

- Trust and company structuring at 25–30% corporate rate captures meaningful ground lost by personal-name sole traders at 47%

- Construction cost inflation hasn’t fully flowed through yet — operators finishing flips in Q2 2026 with pre-procured materials lock in pre-Iran-shock cost bases

The Bear Case: Five Things That Break the Math

- Westpac forecasts two more hikes — 4.70% by year-end, 4.85% peak. Each extra 25bp adds ~$933 of holding cost on a $700K flip

- The APRA DTI cap is permanent, not cyclical. It doesn’t go away if rates fall

- ATO scrutiny on property transactions has intensified post-Bowerman [2023] — the “live in six months and flip” arrangement is higher risk than at any point in the last decade

- Iran-driven oil price shock hasn’t yet appeared in construction cost data — renovation budgets quoted in Q1 will overrun in Q2 and Q3

- A CGT discount Budget cut suppresses buy-and-hold investor appetite at resale — which is exactly who flippers sell to

Watch: Melbourne First Home Buyers Just Borrowed $560K — Most Will Regret It

FAQs

- Is house flipping still profitable in Australia at 4.35%?

Selectively, yes — but only in specific corridors with cosmetic-only renovations, fast execution under 6 months, and proper trust or company structure. After trader-rate tax and GST, a typical Melbourne flip returns single-digit thousands net. - What Melbourne suburbs actually work for flipping in 2026?

The data is pretty clear on this. Frankston SA3 is leading the pack with 11.3% annual growth — that’s the strongest tailwind of any Melbourne corridor right now. Sunbury is sitting at 9% and Brimbank-West at 8.6%. All three are giving flippers enough market movement to absorb holding costs and still walk away with something real. The honest rule of thumb for 2026: if it’s outer corridor with double-digit annual growth, run the numbers. If it’s inner east upper quartile, don’t bother. - Does the 50% CGT discount apply to flipped properties?

Generally no. The ATO classifies repeat flippers as traders under Taxation Ruling TR 92/3, meaning profits are taxed at full marginal rate (up to 47%) as ordinary income. No CGT discount, no main residence exemption. - Is BRRRR better than flipping at 4.35%?

On the modelled comparison, yes — by approximately $185,000 over 5 years. BRRRR retains the asset, compounds capital growth, and preserves the 50% CGT discount on eventual sale. Flipping provides end-of-cycle liquidity but forfeits compounding and the discount.

The NextHouse View

Flipping isn’t dead at 4.35%. The Cotality outer-corridor data is real. The PropTrack 93% headline is real. There are specific corridors — Frankston, Sunbury, Brimbank, Brisbane SE, Perth North, Adelaide North — where the math still works for disciplined operators with the right structure.

But for most operators, most of the time, flipping at 4.35% loses to the BRRRR alternative on the same capital by roughly $185,000 over five years. And that gap widens as rates rise. The single most underestimated problem in Australian flipping right now isn’t the rate hike. It’s the ATO trader classification. Most flippers who think they’re eligible for the 50% CGT discount are simply wrong about their tax position. The correct base case is 47% full marginal rate, no discount, no main residence exemption, and potential GST exposure. Anyone modelling their flip on the CGT discount base case is working with the wrong numbers.

The May 12 Budget CGT review is largely irrelevant to this. Most repeat flippers were never eligible for the discount. The Budget reshapes buy-and-hold investor math; it barely touches the flipping equation.

Disclaimer

This article is produced by NextHouse.com.au for general information and educational purposes only. It is not financial product advice, tax advice, mortgage advice, real estate advice, or legal advice. NextHouse is not licensed to provide personal financial advice. Nothing in this article should be relied upon as a recommendation to buy, sell, hold, renovate, or flip any property or financial product.

All holding cost, repayment, and tax figures are illustrative models at stated assumptions — typically average new variable investor rate at 6.26%, interest-only, 80% LVR, full pass-through, and 47% marginal rate inclusive of 2% Medicare. Outcomes vary materially by lender, loan structure, household income, ATO classification, and individual tax position. The trader-versus-investor and GST discussions are general commentary on ATO Taxation Ruling TR 92/3, Bowerman and Commissioner of Taxation [2023] AATA 3547, and GSTR 2003/3. Classification depends entirely on facts and circumstances.