Nobody expected to be writing this sentence in 2026: the two biggest forces shaping Melbourne property prices right now are a trade war started in Washington and a shooting war in the Middle East. But here we are.

Donald Trump’s tariff regime and the US-Israeli military campaign against Iran — which effectively shut down the Strait of Hormuz in late February — are flowing through to Melbourne’s property market in ways that most buyers haven’t connected yet. Higher construction costs. A forced reversal of the RBA’s rate-cutting cycle. Petrol above $2.38 a litre. And a confidence crisis that’s pushed Melbourne’s “time to buy” sentiment index to its lowest level in years.

Here’s the thing though. The same forces weighing on buyer confidence are simultaneously choking new housing supply in ways that reinforce the structural reasons Melbourne property prices holds its value over the long term. That’s the paradox sitting at the centre of this market right now.

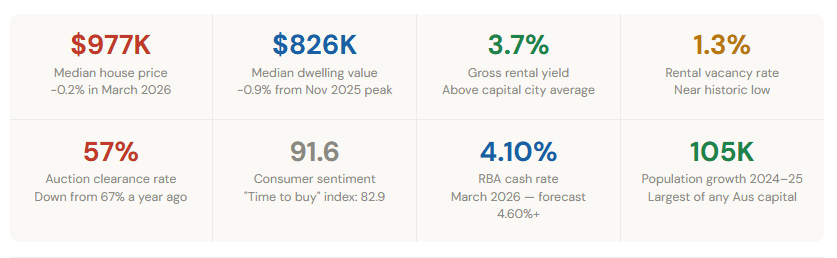

What Are The Melbourne Property Prices Right Now?

Melbourne Residential Property Market Snapshot — April 2026

Source: Cotality HVI March 2026 · NAB Melbourne Property Insights February 2026 · Westpac-Melbourne Institute March 2026

The clearance rate drop from 67% to 57% in twelve months tells a clear story — more sellers, fewer committed buyers. But the rental vacancy sitting at 1.3% and yields strengthening to 3.7% tell a different story running in parallel. This is a market under pressure at the top, holding firm at the bottom.

Part 1: Trump’s Tariffs — How They Actually Reach Melbourne Property?

Most Australians heard about Trump’s tariffs and assumed it was an American problem. It’s not. The transmission into Melbourne’s property market is real, just slightly less direct than it looks.

The sweeping “Liberation Day” tariffs from April 2025 were struck down by the US Supreme Court in February 2026 — but the administration immediately replaced them with a 10% blanket tariff on virtually all imports. Then added sector-specific rates on top of that.

Trump Tariff Rates Active as of April 2026

| Tariff Category | Rate | Status |

| Blanket import tariff | 10% | Active since February 2026 |

| Steel and aluminium | 50% | Restructured and maintained |

| Automobiles and auto parts | 25% | Active |

| Pharmaceuticals (patented) | 100% | Announced first week of April 2026 |

| China, South Korea, Japan goods | 15–54% | Australia’s three largest trading |

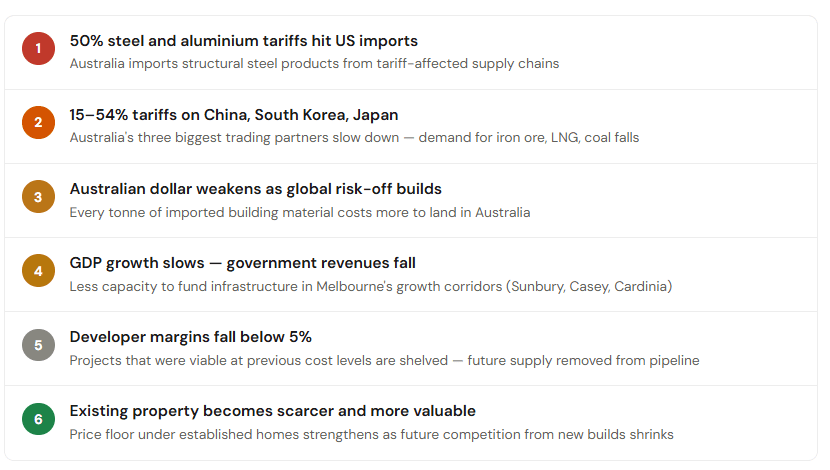

Australia’s direct export exposure to the US is relatively modest — just 4.6% of Australian goods exports go there. So the direct impact is contained. The indirect impact is where it gets serious.

China, Japan, and South Korea face tariffs of 15–54%. When their economies slow down, demand for Australian iron ore, LNG, and coal drops with them. Australia’s Treasury estimates the indirect economic effect is roughly four times the direct tariff impact. Slower national revenue means slower GDP growth, lower government tax receipts, and less capacity to fund the infrastructure — in Sunbury, Casey, and Cardinia — that Melbourne’s growth corridors depend on.

There’s also the materials channel. The 50% steel and aluminium tariff flows into the cost of every beam, every reinforcing rod, and every roofing sheet used in a Melbourne new build. Combined with a weaker Australian dollar — the AUD has softened as global risk sentiment deteriorates — imported materials cost more to land in Australia than they did twelve months ago.

One meaningful offset: the EU-Australia Free Trade Agreement, signed on 24 March 2026, eliminates tariffs on 98% of Australian goods sold into Europe — worth an estimated $10 billion annually in trade diversification.

How the Tariff Chain Reaches Melbourne Property?

Source: DFAT · US Studies Centre April 2026 · EY Australia Trade War Analysis

Part 2: The Iran War — The Bigger, More Immediate Shock

If the tariffs are a slow-building pressure, the Iran war is the immediate shock. And the numbers are extraordinary.

Operation Epic Fury — the US and Israeli military campaign against Iran — began on 28 February 2026. The Strait of Hormuz, through which roughly 20% of global seaborne oil and 25% of global LNG normally transit, has been effectively closed. Vessel traffic through the Strait has fallen 94%. The IEA has described it as the worst energy crisis in history. Diesel exceeded $3 per litre in several capital cities.

Iran War — Impact on Melbourne Property Market

| Impact Area | Data Point | Melbourne Property Effect |

| Brent crude oil price | US$109/barrel (April 2026) vs US$65 (mid-February) | Diesel surcharges on all construction sites |

| Australian petrol price | $2.38/L pre-excise cut; diesel $3+ per litre | Outer suburb buyers face $300–500/month extra in transport |

| Strait of Hormuz traffic | −94% vessel transit drop (IEA, April 2026) | Shipping delays of 10–14 extra days via Cape of Good Hope |

| War-risk insurance | Premiums surged from 0.2% to over 1% of vessel value | Emergency surcharges over US$2,000 per container on Australian routes |

| Australian CPI | 3.7% in February 2026 — before the full oil shock | Forced the RBA to hike rates in February and March 2026 |

| RBA cash rate | 4.10% (March 2026) — forecast 4.60–4.85% | Borrowing capacity shrinking — about $80,000 less on a $600K mortgage vs mid-2025 |

Source: IEA April 2026 · Al Jazeera April 2026 · Marsh Insurance · The Conversation · Crikey March 2026

For Melbourne outer-suburb households already stretching to afford homes in Sunbury, Melton, and Casey, an extra $300–$500 per month in petrol is a material budget hit. Economists are flagging that this may accelerate a demand shift away from car-dependent outer suburbs toward middle-ring suburbs with strong public transport links.

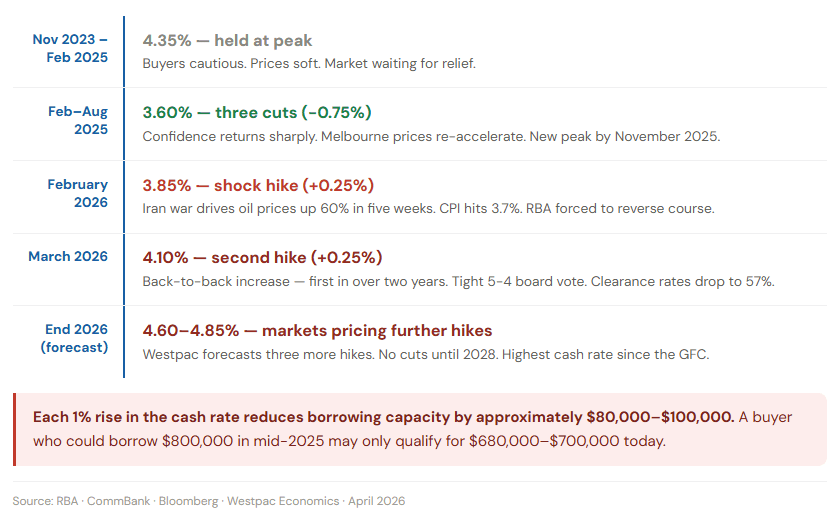

The RBA U-Turn: How the War Reversed the Rate-Cutting Cycle?

This is the single most consequential domestic effect of the Iran war on Melbourne property. Then February 2026 arrived. With CPI at 3.7% and energy costs surging, the RBA had no choice. It hiked in February.

Then hiked again in March — a tight 5-4 board vote — the first back-to-back increases in over two years. The rate-cutting narrative Melbourne property was built on through late 2025 was gone in eight weeks.

Source: RBA · CommBank · Bloomberg · Westpac

What Different Parts of Melbourne Are Doing?

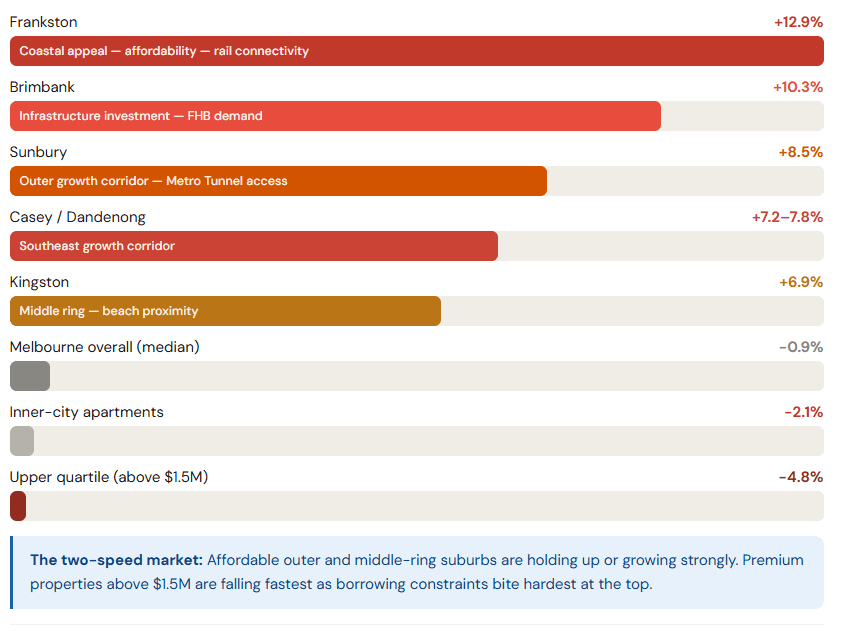

The headline Melbourne number — down 0.9% from the November 2025 peak — hides a market running at two very different speeds.

Melbourne Suburb Performance — Annual Growth to March 2026

Source: Cotality HVI March 2026 · NAB Property Insights · PropertyBuyer.com.au · HtAG Research 2026

The pattern is clear. Affordable outer and middle-ring suburbs with good transport connections are holding up — in some cases strongly. Premium properties at the top of the market are taking the biggest hit because higher rates reduce borrowing capacity fastest where the numbers are largest. The lower quartile is still recording modest monthly gains. The upper quartile is dropping at 0.4% per month.

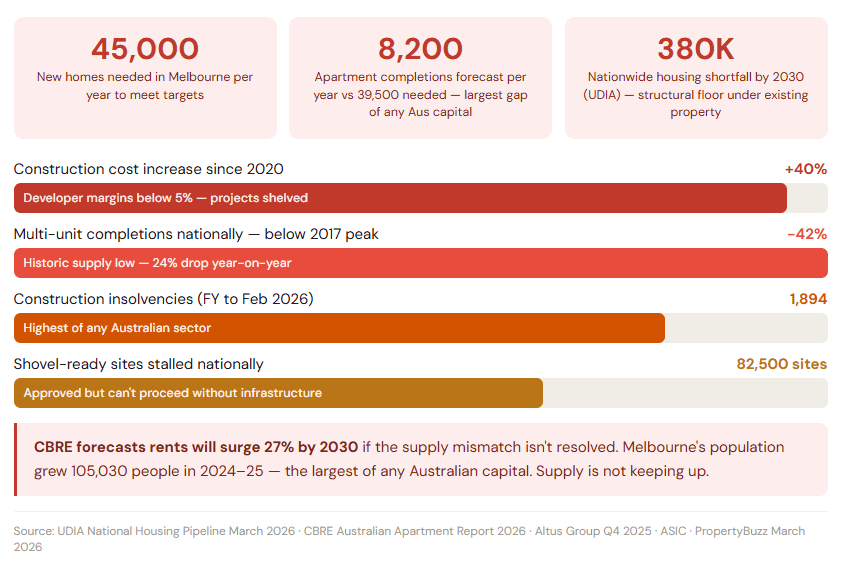

The Supply Paradox: Why the Shortage Gets Worse, Not Better?

Here is the thing that gets lost in all the bad news headlines. The same forces suppressing demand are simultaneously making the housing shortage worse. And the supply problem is structurally far more serious than the demand problem.

Source: UDIA National Housing Pipeline March 2026 · CBRE Australian Apartment Report 2026 · Altus Group Q4 2025

CBRE forecasts apartment construction will average just 8,200 units annually against demand for 39,500 — the largest absolute mismatch of any Australian capital. Construction insolvencies are at record highs. The tariff and war-driven cost surge is making all of this worse. Every building material that goes up in price is another marginal project that doesn’t get built. Every project that doesn’t get built is one more unit of future supply removed from the pipeline. And Melbourne’s population grew by 105,030 people in 2024–25 — the largest increase of any Australian capital. The city is on track to overtake Sydney as Australia’s largest by 2032.

CBRE is forecasting that rents will surge 27% by 2030 if the supply mismatch isn’t resolved. Based on the current trajectory of construction costs and insolvencies, there’s no clear path to resolution by then.

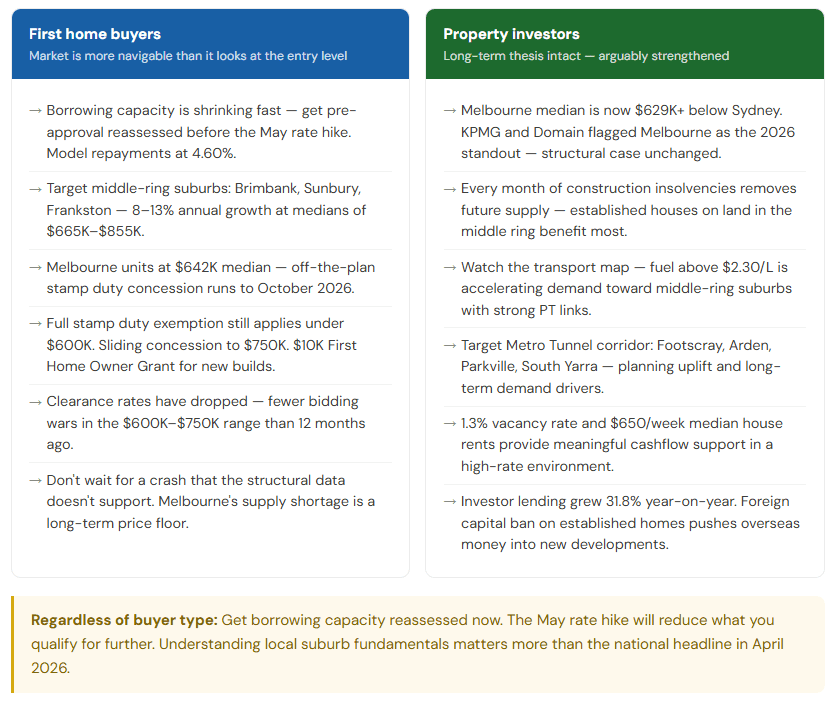

What You Should Actually Do — By Situation?

If You’re a First Home Buyer in Melbourne or Property Investor Here’s what you should do:

The Silver Lining: Australia as a Global Safe Haven

There’s a less visible effect of global turmoil that’s worth understanding. When the world gets unstable, capital moves toward perceived safe havens. Australia’s stable governance, transparent legal system, deep property market, and geographic distance from the Middle East conflict make it attractive when risk is elevated everywhere else.

Foreign investment in Australian real estate and infrastructure rose materially after the Iran war began. The ban on foreign purchases of established homes runs until March 2027 — which channels overseas capital exclusively into new developments, supporting off-the-plan feasibility at exactly the moment it’s most under pressure.

Melbourne house prices: Where Do We Go From Here?

The pressure is real. Rates are rising. Petrol is expensive. Consumer confidence has cratered. Premium properties are falling. Clearance rates are at their weakest in over a year. The paradox is equally real. Every force making buying harder is also making building harder. Every project shelved because of construction costs is one fewer home competing with the existing stock you’re considering buying. Melbourne’s population keeps growing. Vacancy keeps tightening. Rents are heading higher.

The buyers who will look back at 2026 as a great decision are the ones who understood both sides of this story — who bought in the right suburb, at the right price point, with the right long-term view. Not the ones who waited for certainty that never arrived.

Disclaimer: This report is for educational and informational purposes only. It does not constitute financial, investment, or legal advice. Always seek professional advice before making property decisions